Long-run

Encyclopedia

In macroeconomics, the long run is the conceptual time period in which there are no fixed factors of production as to changing the output level by changing the capital stock

or by entering or leaving an industry. The long run contrasts with the short run, in which some factors are variable and others are fixed, constraining entry or exit from an industry. In macroeconomics

, the long run is the period when the general price level

, contractual wage rates, and expectations adjust fully to the state of the economy, in contrast to the short run when these may not fully adjust.

In the long run, firm

s change production levels in response to (expected) economic profits or losses, and the land

, labor, capital goods and entrepreneurship

vary to reach associated long-run average cost. In the simplified case of plant capacity as the only fixed factor, a generic firm can make these changes in the long run:

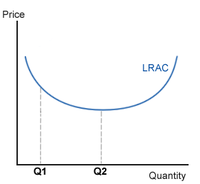

The long run is associated with the long-run average cost (LRAC) curve in microeconomic models along which a firm would minimize its average cost

The long run is associated with the long-run average cost (LRAC) curve in microeconomic models along which a firm would minimize its average cost

(cost per unit) for each respective long-run quantity of output. Long-run marginal cost (LRMC) is the added cost of providing an additional unit of service or commodity

from changing capacity level to reach the lowest cost associated with that extra output. LRMC equalling price is efficient as to resource allocation

in the long run. The concept of long-run cost is also used in determining whether the long-run expected to induce the firm to remain in the industry or shut down production there. In long-run equilibrium of an industry in which perfect competition

prevails, the LRMC = Long run average LRAC at the minimum LRAC and associated output. The shape of the long-run marginal and average costs curves is determined by economies of scale

.

The long run is a planning and implementation stage. Here a firm may decide that it needs to produce on a larger scale by building a new plant or adding a production line. The firm may decide that new technology should be incorporated into its production process. The firm thus considers all its long-run production options and selects the optimal combination of inputs and technology for its long-run purposes. The optimal combination of inputs is the least-cost combination of inputs for desired level of output when all inputs are variable. Once the decisions are made and implemented and production begins, the firm is operating in the short run with fixed and variable inputs.

All production in real time occurs in the short run. The short run is the conceptual time period in which at least one factor of production is fixed in amount and others are variable in amount. Costs that are fixed, say from existing plant size, have no impact on a firm's short-run decisions, since only variable costs and revenues affect short-run profits. Such fixed cost

s raise the associated short-run average cost of an output level over the long-run average cost if the amount of the fixed factor is better suited for a different output level. In the short run, a firm can raise output by increasing the amount of the variable factor(s), say labor through overtime.

A generic firm already producing in an industry can make three changes in the short run as a response to reach a posited equilibrium:

In the short run, a profit-maximizing

firm will:

The transition from the short run to the long run may be done by considering some short-run equilibrium that is also a long-run equilibrium as to supply and demand

, then comparing that state against a new short-run and long-run equilibrium state from a change that disturbs equilibrium, say in the sales-tax rate, tracing out the short-run adjustment first, then the long-run adjustment. Each is an example of comparative statics

. Alfred Marshall

(1890) pioneered in comparative-static period analysis. He distinguished between the temporary or market period (with output fixed), the short period, and the long period. "Classic" contemporary graphical and formal treatments include those of Jacob Viner

(1931), John Hicks

(1939), and Paul Samuelson

(1947).

The law of diminishing marginal returns to a variable factor applies to the short run. It posits an effect of decreased added or marginal product

of from variable factors, which increases the supply price of added output. The law is related to a positive slope of the short-run marginal-cost curve.

The usage of 'long run' and 'short run' in macroeconomics

differs somewhat from the above microeconomic usage. J.M. Keynes (1936) emphasized fundamental factors of a market economy that might result in prolonged periods away from full-employment

. In later macro usage, the long run is the period in which the price level

for the economy is completely flexible as to shifts in aggregate demand

and aggregate supply

. In addition there is full mobility of labor and capital between sectors of the economy and full capital

mobility between nations. In the short run none of these conditions need fully hold. The price is sticky

or fixed as to changes in aggregate demand or supply, capital is not fully mobile between sectors, and capital is not fully mobile to interest rate differences among countries & fixed exchange rates.

A famous critique of neglecting short-run analysis was by John Maynard Keynes

, who wrote that "In the long run, we are all dead," referring to the long-run proposition of the quantity theory of, for example, a doubling of the money supply

doubling the price level

.

Capital (economics)

In economics, capital, capital goods, or real capital refers to already-produced durable goods used in production of goods or services. The capital goods are not significantly consumed, though they may depreciate in the production process...

or by entering or leaving an industry. The long run contrasts with the short run, in which some factors are variable and others are fixed, constraining entry or exit from an industry. In macroeconomics

Macroeconomics

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of the whole economy. This includes a national, regional, or global economy...

, the long run is the period when the general price level

Price level

A price level is a hypothetical measure of overall prices for some set of goods and services, in a given region during a given interval, normalized relative to some base set...

, contractual wage rates, and expectations adjust fully to the state of the economy, in contrast to the short run when these may not fully adjust.

In the long run, firm

Business

A business is an organization engaged in the trade of goods, services, or both to consumers. Businesses are predominant in capitalist economies, where most of them are privately owned and administered to earn profit to increase the wealth of their owners. Businesses may also be not-for-profit...

s change production levels in response to (expected) economic profits or losses, and the land

Land (economics)

In economics, land comprises all naturally occurring resources whose supply is inherently fixed. Examples are any and all particular geographical locations, mineral deposits, and even geostationary orbit locations and portions of the electromagnetic spectrum. Natural resources are fundamental to...

, labor, capital goods and entrepreneurship

Entrepreneurship

Entrepreneurship is the act of being an entrepreneur, which can be defined as "one who undertakes innovations, finance and business acumen in an effort to transform innovations into economic goods". This may result in new organizations or may be part of revitalizing mature organizations in response...

vary to reach associated long-run average cost. In the simplified case of plant capacity as the only fixed factor, a generic firm can make these changes in the long run:

- enter an industry in response to (expected) profits

- leave an industry in response to losses

- increase its plant in response to profits

- decrease its plant in response to losses.

Average cost

In economics, average cost or unit cost is equal to total cost divided by the number of goods produced . It is also equal to the sum of average variable costs plus average fixed costs...

(cost per unit) for each respective long-run quantity of output. Long-run marginal cost (LRMC) is the added cost of providing an additional unit of service or commodity

Commodity

In economics, a commodity is the generic term for any marketable item produced to satisfy wants or needs. Economic commodities comprise goods and services....

from changing capacity level to reach the lowest cost associated with that extra output. LRMC equalling price is efficient as to resource allocation

Resource allocation

Resource allocation is used to assign the available resources in an economic way. It is part of resource management. In project management, resource allocation is the scheduling of activities and the resources required by those activities while taking into consideration both the resource...

in the long run. The concept of long-run cost is also used in determining whether the long-run expected to induce the firm to remain in the industry or shut down production there. In long-run equilibrium of an industry in which perfect competition

Perfect competition

In economic theory, perfect competition describes markets such that no participants are large enough to have the market power to set the price of a homogeneous product. Because the conditions for perfect competition are strict, there are few if any perfectly competitive markets...

prevails, the LRMC = Long run average LRAC at the minimum LRAC and associated output. The shape of the long-run marginal and average costs curves is determined by economies of scale

Economies of scale

Economies of scale, in microeconomics, refers to the cost advantages that an enterprise obtains due to expansion. There are factors that cause a producer’s average cost per unit to fall as the scale of output is increased. "Economies of scale" is a long run concept and refers to reductions in unit...

.

The long run is a planning and implementation stage. Here a firm may decide that it needs to produce on a larger scale by building a new plant or adding a production line. The firm may decide that new technology should be incorporated into its production process. The firm thus considers all its long-run production options and selects the optimal combination of inputs and technology for its long-run purposes. The optimal combination of inputs is the least-cost combination of inputs for desired level of output when all inputs are variable. Once the decisions are made and implemented and production begins, the firm is operating in the short run with fixed and variable inputs.

All production in real time occurs in the short run. The short run is the conceptual time period in which at least one factor of production is fixed in amount and others are variable in amount. Costs that are fixed, say from existing plant size, have no impact on a firm's short-run decisions, since only variable costs and revenues affect short-run profits. Such fixed cost

Fixed cost

In economics, fixed costs are business expenses that are not dependent on the level of goods or services produced by the business. They tend to be time-related, such as salaries or rents being paid per month, and are often referred to as overhead costs...

s raise the associated short-run average cost of an output level over the long-run average cost if the amount of the fixed factor is better suited for a different output level. In the short run, a firm can raise output by increasing the amount of the variable factor(s), say labor through overtime.

A generic firm already producing in an industry can make three changes in the short run as a response to reach a posited equilibrium:

- increase production

- decrease production

- shut down.

In the short run, a profit-maximizing

Profit maximization

In economics, profit maximization is the process by which a firm determines the price and output level that returns the greatest profit. There are several approaches to this problem...

firm will:

- increase production if marginal costMarginal costIn economics and finance, marginal cost is the change in total cost that arises when the quantity produced changes by one unit. That is, it is the cost of producing one more unit of a good...

is less than marginal revenueMarginal revenueIn microeconomics, marginal revenue is the extra revenue that an additional unit of product will bring. It is the additional income from selling one more unit of a good; sometimes equal to price...

(added revenue per additional unit of output; - decrease production if marginal costMarginal costIn economics and finance, marginal cost is the change in total cost that arises when the quantity produced changes by one unit. That is, it is the cost of producing one more unit of a good...

is greater than marginal revenueMarginal revenueIn microeconomics, marginal revenue is the extra revenue that an additional unit of product will bring. It is the additional income from selling one more unit of a good; sometimes equal to price...

; - continue producing if average variable costAverage variable costAverage variable cost is an economics term that refers to a firm's variable costs divided by the quantity of output produced...

is less than pricePrice-Definition:In ordinary usage, price is the quantity of payment or compensation given by one party to another in return for goods or services.In modern economies, prices are generally expressed in units of some form of currency...

per unit, even if average total cost is greater than pricePrice-Definition:In ordinary usage, price is the quantity of payment or compensation given by one party to another in return for goods or services.In modern economies, prices are generally expressed in units of some form of currency...

; - shut down if average variable costAverage variable costAverage variable cost is an economics term that refers to a firm's variable costs divided by the quantity of output produced...

is greater than pricePrice-Definition:In ordinary usage, price is the quantity of payment or compensation given by one party to another in return for goods or services.In modern economies, prices are generally expressed in units of some form of currency...

at each level of output.

The transition from the short run to the long run may be done by considering some short-run equilibrium that is also a long-run equilibrium as to supply and demand

Supply and demand

Supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good will vary until it settles at a point where the quantity demanded by consumers will equal the quantity supplied by producers , resulting in an...

, then comparing that state against a new short-run and long-run equilibrium state from a change that disturbs equilibrium, say in the sales-tax rate, tracing out the short-run adjustment first, then the long-run adjustment. Each is an example of comparative statics

Comparative statics

In economics, comparative statics is the comparison of two different economic outcomes, before and after a change in some underlying exogenous parameter....

. Alfred Marshall

Alfred Marshall

Alfred Marshall was an Englishman and one of the most influential economists of his time. His book, Principles of Economics , was the dominant economic textbook in England for many years...

(1890) pioneered in comparative-static period analysis. He distinguished between the temporary or market period (with output fixed), the short period, and the long period. "Classic" contemporary graphical and formal treatments include those of Jacob Viner

Jacob Viner

Jacob Viner was a Canadian economist and is considered with Frank Knight and Henry Simons one of the "inspiring" mentors of the early Chicago School of Economics in the 1930s: he was one of the leading figures of the Chicago faculty.- Biography :Viner was born in 1892 in Montreal, Quebec to...

(1931), John Hicks

John Hicks

Sir John Richard Hicks was a British economist and one of the most important and influential economists of the twentieth century. The most familiar of his many contributions in the field of economics were his statement of consumer demand theory in microeconomics, and the IS/LM model , which...

(1939), and Paul Samuelson

Paul Samuelson

Paul Anthony Samuelson was an American economist, and the first American to win the Nobel Memorial Prize in Economic Sciences. The Swedish Royal Academies stated, when awarding the prize, that he "has done more than any other contemporary economist to raise the level of scientific analysis in...

(1947).

The law of diminishing marginal returns to a variable factor applies to the short run. It posits an effect of decreased added or marginal product

Marginal product

In economics and in particular neoclassical economics, the marginal product or marginal physical product of an input is the extra output that can be produced by using one more unit of the input , assuming that the quantities of no other inputs to production...

of from variable factors, which increases the supply price of added output. The law is related to a positive slope of the short-run marginal-cost curve.

The usage of 'long run' and 'short run' in macroeconomics

Macroeconomics

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of the whole economy. This includes a national, regional, or global economy...

differs somewhat from the above microeconomic usage. J.M. Keynes (1936) emphasized fundamental factors of a market economy that might result in prolonged periods away from full-employment

Full employment

In macroeconomics, full employment is a condition of the national economy, where all or nearly all persons willing and able to work at the prevailing wages and working conditions are able to do so....

. In later macro usage, the long run is the period in which the price level

Price level

A price level is a hypothetical measure of overall prices for some set of goods and services, in a given region during a given interval, normalized relative to some base set...

for the economy is completely flexible as to shifts in aggregate demand

Aggregate demand

In macroeconomics, aggregate demand is the total demand for final goods and services in the economy at a given time and price level. It is the amount of goods and services in the economy that will be purchased at all possible price levels. This is the demand for the gross domestic product of a...

and aggregate supply

Aggregate supply

In economics, aggregate supply is the total supply of goods and services that firms in a national economy plan on selling during a specific time period...

. In addition there is full mobility of labor and capital between sectors of the economy and full capital

Capital (economics)

In economics, capital, capital goods, or real capital refers to already-produced durable goods used in production of goods or services. The capital goods are not significantly consumed, though they may depreciate in the production process...

mobility between nations. In the short run none of these conditions need fully hold. The price is sticky

Sticky (economics)

Sticky, in the social sciences and particularly economics, describes a situation in which a variable is resistant to change. Sticky prices are an important part of macroeconomic theory since they may be used to explain why markets might not reach equilibrium right away. Nominal wages are often said...

or fixed as to changes in aggregate demand or supply, capital is not fully mobile between sectors, and capital is not fully mobile to interest rate differences among countries & fixed exchange rates.

A famous critique of neglecting short-run analysis was by John Maynard Keynes

John Maynard Keynes

John Maynard Keynes, Baron Keynes of Tilton, CB FBA , was a British economist whose ideas have profoundly affected the theory and practice of modern macroeconomics, as well as the economic policies of governments...

, who wrote that "In the long run, we are all dead," referring to the long-run proposition of the quantity theory of, for example, a doubling of the money supply

Money supply

In economics, the money supply or money stock, is the total amount of money available in an economy at a specific time. There are several ways to define "money," but standard measures usually include currency in circulation and demand deposits .Money supply data are recorded and published, usually...

doubling the price level

Price level

A price level is a hypothetical measure of overall prices for some set of goods and services, in a given region during a given interval, normalized relative to some base set...

.