Tax protester constitutional arguments

Encyclopedia

Tax protester constitutional arguments are assertions that the imposition of the federal income tax

violates the United States Constitution

. These kinds of tax protester arguments

are distinguished from related statutory arguments

and conspiracy arguments

, which presuppose the constitutionality of the income tax. Although the most frequent Constitutional arguments are directed towards the validity and effect of the Sixteenth Amendment

, arguments exist that the income tax violates some other provision of the Constitution; or that some other provision, that would prevent the assessment of the income tax, was ratified but wrongfully excluded from the Constitution.

Other constitutional amendment arguments have been raised by tax protesters. Some argue that imposition of the income tax violates the First Amendment

freedom of speech

and freedom of religion

. Protesters argue that the income tax violates the Fifth Amendment

right against self-incrimination

, the Takings Clause, or the right that no person shall be "deprived of life, liberty, or property, without due process of law". Tax protesters have argued that income taxes impose involuntary servitude

in violation of the Thirteenth Amendment

. Some tax protesters argue that Americans are citizens of the individual states as opposed to citizens of the United States, as the Fourteenth Amendment

was not properly ratified. Another argument is a missing amendment to the Constitution, known as the Titles of Nobility Amendment

, which precedes the current Thirteenth Amendment. Another argument raised is that because the federal income tax is progressive

, the discriminations and inequalities created by the tax should render the tax unconstitutional. These arguments have been rejected by the courts.

The authority of the federal government has been challenged by protesters, arguing that they should be immune from federal income taxation because they are sovereign individuals or natural individuals, have not requested a privilege or benefit from the government, or are outside the "federal zone" (D.C.

and various federal enclaves such as military bases). Neither the U.S. Supreme Court nor any other federal court has ruled that an income tax imposed under the Internal Revenue Code

of 1986 is unconstitutional. Under the Supreme Court ruling in Cheek v. United States

, a defendant in a tax evasion

prosecution who has made arguments that the federal income tax laws are unconstitutional may have the arguments turned against him (or her). Such arguments, even if based on honestly held beliefs, may constitute evidence that helps the prosecutor prove willfulness, one of the elements of tax evasion.

freedom of speech

because it requires the subject of the tax to write information on a tax return; or violates freedom of religion

if the subject of the tax claims some religious objection to the payment of taxes, particularly if the subject styles himself or herself as a Reverend, Minister, or other religious office-holder. While the Internal Revenue Code

makes an exemption for churches and other religious institutions, it makes only special tax codes and deductions, not exceptions, for religious professionals. The United States Supreme Court held in 1878 Reynolds v. United States

, that a religious belief, however strongly held, does not exempt the believer from adhering to general laws.

Other protesters argue that the Fifth Amendment

Other protesters argue that the Fifth Amendment

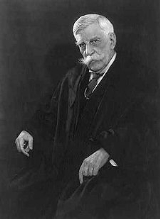

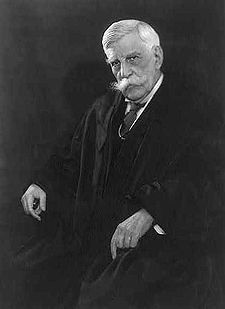

right against self-incrimination allows an individual to refuse to file an income tax return calling for information that could lead to a conviction for criminal acts from which the income was derived, or for the crime of not paying the tax itself. In response, the courts generally refer to the case of United States v. Sullivan, where Justice Oliver Wendell Holmes

wrote:

. The takings argument and variations of this argument have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

Fifth Amendment "due process" arguments by tax protesters were rejected by the United States Court of Appeals for the Third Circuit in Kahn v. United States, by the United States Court of Appeals for the Fifth Circuit in Anderson v. United States, by the United States Court of Appeals for the Seventh Circuit in Cameron v. Internal Revenue Serv., by the United States Court of Appeals for the Eighth Circuit in Baskin v. United States, by the United States Court of Appeals for the Ninth Circuit in Jolly v. United States, and by the United States Court of Appeals for the Tenth Circuit in Martinez v. Internal Revenue Serv.

" in violation of the Thirteenth Amendment

. That argument was ruled to be without merit in Porth v. Brodrick, United States Collector of Internal Revenue for the State of Kansas. The involuntary servitude argument, and variations of this argument, have been officially identified as legally frivolous

federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

states:

Notably, some tax protesters contend that the Fourteenth Amendment itself was never properly ratified, under the theory that the governments of southern states that supported the post-Civil War amendments were not representative of the people.

Courts have uniformly held that this argument that the Fourteenth Amendment divested state citizens of U.S. citizenship is plainly incorrect. In Kantor v. Wellesley Galleries, Ltd., the court explained that "[w]hile the Fourteenth Amendment does not create a national citizenship, it has the effect of making that citizenship 'paramount and dominant' instead of 'derivative and dependent' upon state citizenship". See also United States v. Ward,Fox v. Commissioner, and United States v. Baker.

was not propertly ratified, and that all laws passed by Congress since the year 1919 (which was not the year of ratification) are invalid. The Trohimovich case involved a criminal contempt charge against the taxpayer in connection with a failure to obey a subpoena to produce books and records needed for the trial of the case. The United States Tax Court stated:

The court rejected the taxpayer's arguments, and ordered that "he be imprisoned for 30 days as punishment" for criminal contempt in failing to obey court orders or subpoenas.

or "TONA" precedes the current Thirteenth Amendment

; the missing amendment purportedly would have divested the citizenship of any person receiving a title of nobility. Therefore, actions taken by lawyers and judges, who use the title 'Esquire

' (which some protesters claim is a title of nobility), are monarchical, and therefore unconstitutional. This contention, rarely raised before courts, was most recently addressed in Campion v. Towns, No.CV-04-1516PHX-ROS, *2 n.1

(D. Ariz. 2005) as a defense to a charge of tax evasion. The court replied:

s or "natural individuals," or on the ground that they have not requested a privilege or benefit from the government. These kinds of arguments have been ruled without merit. For example, in the case of Lovell v. United States the United States Court of Appeals for the Seventh Circuit stated:

The Court of Appeals in Lovell affirmed a U.S. District Court order upholding a frivolous return penalty under . Similarly, in United States v. Sloan, the taxpayer's contention — that he is "not a citizen of the United States, but rather, that he is a freeborn, natural individual, a citizen of the State of Indiana, and a 'master'—not 'servant'—of his government" — was ruled to be not a legal ground for the argument that the taxpayer was not subject to the federal tax laws; the tax evasion conviction was upheld by the United States Court of Appeals for the Seventh Circuit. Similarly, the United States Court of Appeals for the Third Circuit stated, in Powers v. Commissioner: "Powers [the taxpayer] contends that either he is immune from the tax laws, or he is a 'slave' to the federal government. This false choice is a creature of Powers' tax protester ideology, not the laws of this Republic." Similarly, in 2008 the United States Court of Appeals for the Tenth Circuit rejected a taxpayer's argument that gains of an individual's labor could be taxed only if the gains were received from a "federal venue". In that case, the taxpayer's argument -- that the IRS had no ability to impose a tax on the taxpayer because he was a citizen "of the several states," but not a "federal U.S. citizen" -- was ruled to be frivolous.

Variations of the argument that an individual is a “sovereign” have been rejected in tax cases such as United States v. Hart, Risner v. Commissioner, Maxwell v. Snow, Rowe v. Internal Revenue Serv., Cobin v. Commissioner, and Glavin v. United States.

The argument that an individual who received Form W-2 wages or other compensation is not subject to federal income tax because the individual has "neither requested, obtained, nor exercised any privilege from an agency of government" was ruled frivolous by the United States Court of Appeals for the First Circuit in Sullivan v. United States and again in Kelly v. United States. See also United States v. Buras (argument that the taxpayer can be subject to an excise tax only if he benefits from a "privilege extended by a government agency" was rejected).

The argument that an individual who received Form W-2 wages is not subject to federal income tax unless the tax is imposed in connection with "government granted privileges" was ruled frivolous by the United States Court of Appeals for the Seventh Circuit in Coleman v. Commissioner. The argument that an individual who received Form W-2 wages is not subject to federal income tax unless the taxpayer enjoys a "grant of privilege or franchise" was ruled frivolous by the United States Court of Appeals for the Eighth Circuit in May v. Commissioner. The argument that an individual who received Form W-2 wages is not subject to federal income tax unless the taxpayer has obtained a "privilege from a governmental agency" was ruled frivolous by the United States Court of Appeals for the Ninth Circuit in Olson v. United States, and by the United States Court of Appeals for the Tenth Circuit in Prout v. United States.

In the case of Steward Machine Company v. Davis

, the Supreme Court rejected the argument that "the relation of employment is one so essential to the pursuit of happiness that it may not be burdened with a tax," and upheld the validity of the Social Security tax. The Court stated: ". . . natural rights, so called, are as much subject to taxation as rights of less importance. An excise is not limited to vocations or activities that may be prohibited altogether. It is not limited to those that are the outcome of a franchise. It extends to vocations or activities pursued as of common right.".

Regarding the taxability of income in connection with events or activities not involving a government privilege or franchise, the United States Supreme Court stated in United States v. Sullivan that gains from illegal traffic in liquor are subject to the Federal income tax. The U.S. Supreme Court ruled in Rutkin v. United States that the receipt of money obtained by extortion is taxable as income to the wrongdoer.. The U.S. Supreme Court ruled in James v. United States that the receipt of money obtained through embezzlement is taxable as income to the wrongdoer, even though the wrongdoer is required to return the money to its owner.

The argument that a person's income is not taxed when the person rejects or renounces United States citizenship because the person claims to be a citizen exclusively of a state, and variations of this argument, have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

This argument is based in part on the U.S. Supreme Court decision in the case of United States v. Bevans. In Bevans, the parties argued over whether a federal court in Massachusetts had jurisdiction over the case of a U.S. Marine charged with a murder that occurred on a ship in Boston Harbor. No issues regarding federal income taxation or the Internal Revenue Code were presented to or decided by the Court in the Bevans case. The Internal Revenue Code and the Internal Revenue Service did not yet exist in 1818, when the Bevans murder case was decided.

The Clause 17 argument was specifically rejected in the case of United States v. Sato:

The Clause 17 argument was also unsuccessful in Celauro v. United States, Internal Revenue Service.

Some tax protesters contend that the U.S. Supreme Court decision in Caha v. United States restricts the jurisdiction of the federal government to impose income taxes inside the "states", based on the following language from the Court’s opinion:

Some tax protesters contend that the Court's reference to "those matters" restricted the federal government's jurisdiction over matters of taxation. Caha is not a tax case. The reference to "this statute" was a reference to a perjury statute. The Caha case involved a perjury conviction where the defendant unsuccessfully argued that the federal court had no jurisdiction over a prosecution for the crime of perjury committed in a proceeding in a land office at Kingfisher, Oklahoma regarding ownership of real estate.

The reference in Caha to the "laws of congress in respect to those matters" was a reference to the matters of preservation of the peace and the protection of person and property. The Court in Caha rejected the argument that the federal courts had no jurisdiction to hear a case under the perjury statute, and the defendant's conviction was affirmed. No issues involving the power to impose and enforce federal taxes in the fifty states were presented to or decided by the court in Caha.

The courts have uniformly rejected the "federal zone" argument that congressional authority to impose an income tax is limited to the District of Columbia, forts, magazines, arsenals, or dockyards, etc. See, for example, United States v. Mundt; Nelsen v. Commissioner; Abbs v. Imhoff.

The above verbiage is immediately followed in the text of the case by this sentence:

In Doyle, the taxpayer was a corporation engaged in the manufacture of lumber. In 1903, the taxpayer purchased certain timber land at a cost of about 20 $/acre. As of December 31, 1908, the value of the land had increased to about 40 $/acre. The Corporation Excise Tax Act of 1909 was enacted on August 5, 1909, and was effective retroactively to January 1, 1909. For the years 1909 through 1912, the taxpayer filed tax returns under the 1909 Act, showing gross receipts from the sale of manufactured lumber and, in arriving at the amount of net income subject to tax under the 1909 Act, deducted an amount based on the $40-per-acre value, rather than the actual cost of about $20 per acre. The Commissioner of Internal Revenue argued that the taxpayer should be able to deduct only an amount based on the taxpayer’s historical cost basis of $20, rather than the $40 fair market value at the time the 1909 Act became effective. (Essentially, if the taxpayer were allowed to use the $40 per acre value as its basis rather than the actual $20 historical cost basis, a portion of the taxpayer’s gain — the increase in value from 1903 to December 31, 1908 — would go untaxed.)

The U.S. Supreme Court ruled that under the 1909 Act — which had become effective January 1, 1909 — the taxpayer should be taxed only on the increase in value after 1908. Increases in value prior to the effective date of the statute were not to be taxed under the terms of that statute. Thus, the taxpayer was entitled to deduct, from its gross receipts from the sale of finished lumber, a basis amount computed with reference to the $40 per acre value as of December 31, 1908. Doyle is a case involving statutory (not constitutional) interpretation. In this case, the Court was interpreting the 1909 statute. Although some tax protesters cite this case for an argument about the constitutional definition of income as excluding income of individuals, no issues involving the constitutional definition of income, or of income under any other tax statutes, were presented to or decided by the Court.

The case is also notable for the fact that it involved a retroactively imposed tax. The taxpayer did not argue — and the Court did not rule — that as a general proposition taxes could not be imposed retroactively. Indeed, the tax in this case was imposed retroactively; the statute was enacted in August 1909 but was made effective retroactively to January 1, 1909.

The Court in Merchants' Loan was specifically interpreting a 1916 statute imposing income taxes on individuals and estates (among other kinds of entities), and not the 1909 corporate tax statute. The taxpayer in Merchants' Loan was not a corporation but was the "Estate of Arthur Ryerson, Deceased". The Court was not presented with (and did not decide) any issue involving the taxability of "corporate profits" or "corporate gains" or any other kind of income except the gain on the sale of the stock by the "Estate of Arthur Ryerson, Deceased". The terms "corporate profit" and "corporate gain" are not found in the text of the Court’s decision in Merchants’ Loan. In Merchants' Loan, the Supreme Court ruled that under the Sixteenth Amendment to the United States Constitution and the 1916 tax statute applicable at the time, a gain on a sale of stock by the estate of a deceased person is included in the income of that estate, and is therefore taxable to that estate for federal income tax purposes.

The Merchants' Loan argument has been litigated by tax protesters several times, and the courts have uniformly rejected the argument that income consists only of corporate profits. See, for example: Cameron v. Internal Revenue Serv., Stoewer v. Commissioner, Reinhart v. United States, Fink v. Commissioner; Flathers v. Commissioner; Schroeder v. Commissioner; Sherwood v. Commissioner; and Ho v. Commissioner. Tax protesters — who have lost every case using Merchants' Loan for the theory that only "corporate profits" could be taxable — are citing a case where the U.S. Supreme Court ruled that the income of a non-corporate taxpayer is taxable. Neither the United States Supreme Court nor any other federal court has ever ruled that under the Internal Revenue Code the term "income" means only the income of a corporation for federal income tax purposes.

Some tax protesters have cited the Supreme Court case of Flint v. Stone Tracy Co.

for the argument that only corporate profits or income can be taxed, using the following quotation:

In Flint v. Stone Tracy Co., the U.S. Supreme Court ruled that the corporation tax act of 1909 did not violate the constitutional requirement that revenue measures originate in the U.S. House of Representatives. The Court did not rule that excise taxes consisted only of taxes on corporations and corporate privileges, to the exclusion of taxes on individuals (natural persons). The issue of the validity of an income tax imposed on individuals was neither presented to the Court nor decided by the Court.

The courts have rejected the argument that Flint v. Stone Tracy Co. can be used to avoid taxation of wages. For example, in Parker v. Commissioner, a case where a taxpayer unsuccessfully argued that wages were not taxable, the United States Court of Appeals for the Fifth Circuit stated (in part):

The argument that only corporations are subject to federal income tax, and variations of this argument, have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

In Murphy v. Internal Revenue Serv.

, the United States Court of Appeals for the District of Columbia Circuit ruled that a personal injury award received by a taxpayer was "within the reach of the congressional power to tax under Article I, Section 8 of the Constitution" — even if the award was "not income within the meaning of the Sixteenth Amendment".

(i.e., because the marginal tax rates increase, or progress, as the level of taxable income increases), the discriminations and inequalities created by the tax should render the tax unconstitutional. This argument was rejected by the United States Supreme Court in two companion cases — with respect to the income tax on individuals in Thorne v. Anderson, and with respect to the income tax on corporations in Tyee Realty Co. v. Anderson.

" as used in the Sixteenth Amendment cannot be interpreted as applying to wage

s; that wages are not income

because labor is exchanged for them; that taxing wages violates individuals' right to property; and several others.

Another protester argument is that the U.S. Constitution authorizes the income tax only on income derived from activities that are government-licensed or otherwise specially protected. The courts have rejected this theory, ruling that "Congress has taxed compensation for services, without any regard for whether that compensation is derived from government-licensed or specially protected activities, [ . . . ] and this has been construed to cover earnings from labor."

Robert L. Schulz and his We the People Foundation

take the positions that the government "is clearly prohibited from doing what it is doing – taxing the salaries, wages and compensation of the working men and women of this country and forcing the business entities that utilize the labor of ordinary American citizens to withhold and turn over to the IRS a part of the earnings of those workers" and "that the federal government DOES NOT possess ANY legal authority -- statutory or Constitutional -- to tax the wages or salaries of American workers."

Similarly, tax protester Tom Cryer

, who was acquitted of willful failure to file U.S. Federal income tax returns in a timely fashion, argues that "the law does not tax [a person's] wages", and that the federal government cannot tax "[m]oney that you earned [and] paid for with your labor and industry" because "the Constitution does not allow the federal government to tax those earnings" (referring to "wages, salaries and fees that [a person] earn[s] for [himself]").

Arguments about the taxability of compensation for personal services, whether called wages, salary, or some other term, may be either constitutional arguments as in United States v. Connor (see below) or statutory arguments as in Cheek v. United States

,, depending on the details of the argument. For purposes of presentation, these arguments are summarized here rather than in the article Tax protester statutory arguments

. The rest of this section explains these arguments in more detail.

The quoted material by Dave Champion is false; it does not appear in the Court's decision. In Evans v. Gore, the U.S. Supreme Court actually did rule that a federal income tax on certain income of federal judges was unconstitutional. The Evans v. Gore ruling has been interpreted as barring application of the Federal income tax to a Federal judge who had been appointed prior to the enactment of the tax. This was the Court's year 1920 interpretation of the "Compensation Clause", the rule that Federal judges "shall, at stated Times, receive for their Services a Compensation, which shall not be diminished during their Continuance in Office" under Article III, section 1 of the U.S. Constitution. The decision in Evans v. Gore was eviscerated in the 1939 U.S. Supreme Court decision of O'Malley v. Woodrough, and was expressly overruled by the U.S. Supreme Court itself in 2001, in the case of United States v. Hatter. In Hatter, the Supreme Court stated: "We now overrule Evans insofar as it holds that the Compensation Clause forbids Congress to apply a generally applicable, nondiscriminatory tax to the salaries of federal judges, whether or not they were appointed before enactment of the tax."

Neither the Supreme Court nor any other federal court has ever ruled that the Sixteenth Amendment (or any other part of the Constitution) does not authorize a Federal income tax on compensation for personal services.

This case began in the United States District Court for the Southern District of New York. In the decision in that court, the trial court judge stated: "I do not think that 'income' as used in the statute, should be given a meaning so as to include everything that comes in." The case did not involve compensation for labor or services. Instead, the case involved the federal income tax treatment of dividends paid by the Central Pacific Railway Company to its parent company, the Southern Pacific Company, which owned 100% of the stock of Central Pacific Railway Company. The District Court ruled that the dividends were taxable to the Southern Pacific Company. This decision was reversed by the Supreme Court.

What the U.S. Supreme Court actually said was:

In Southern Pacific Company v. Lowe, the Supreme Court ruled that where a shareholder receives a dividend representing earnings of a corporation realized by the corporation prior to January 1, 1913, the dividend is not includible in the gross income of the shareholder for purposes of the Federal Income Tax Act of 1913, Ch. 16, 38 Stat. 114 (Oct. 3, 1913). No issues involving the definition of income with respect to wages, salary or other compensation for labor were decided by the Court.

This material alleged to be a quotation does not appear in the text of the case at all. Also, the words "wages" and "salaries" are not found anywhere in the text, and there is no ruling in that case that the federal income tax statutes apply only to "corporations." The Colonial Pipeline case actually involved the Louisiana corporate franchise tax, not a federal tax. The validity of the Louisiana franchise tax was upheld by the U.S. Supreme Court in this case. No issues involving the validity or applicability of federal income taxes were presented to, mentioned by, or decided by the Supreme Court in the Colonial Pipeline case.

—incorrectly attribute to the U.S. Supreme Court the following language in connection with the leading tax case of Lucas v. Earl

:

This language is not from the Court’s opinion in Lucas v. Earl. Instead, it is an almost direct quotation from page 17 of the taxpayer's brief filed in the case. Guy C. Earl was the taxpayer, and the brief was written by Earl’s attorneys: Warren Olney, Jr., J.M. Mannon, Jr., and Henry D. Costigan. In some printed versions of the case, this statement and other quotations and paraphrases from pages 8, 10, 14, 15, 17, and 18 of the taxpayer's brief are re-printed as a headnote or syllabus above the opinion of the Court. In the case reprints that include this headnote (and many of them do not even show it), these excerpts are not clearly identified as being from the taxpayer's brief. A person not trained in analysis of legal materials would not necessarily know that this verbiage, like any headnote or syllabus, is not part of the Court’s opinion, perhaps leading to the confusion about the source of the quotation. As explained below, the Supreme Court rejected the arguments in the quotation, and the taxpayer lost the case.

Lucas v. Earl is a leading case in the area of U.S. income taxation, and stands for the Anticipatory Assignment of Income Doctrine

. In the case, Mr. Earl was arguing that because he and his wife, in the year 1901, had made a legally valid assignment agreement (for state law purposes) to have his then-current and after-acquired income (which was earned solely by him) be treated as the income of both him and his wife as joint tenants with right of survivorship, the assignment agreement should also determine the federal income tax effect of the income he earned (i.e., only half the income should be taxed to him).

The U.S. Supreme Court rejected that argument, essentially ruling that under federal income tax law all the future income earned by Mr. Earl was taxable to him at the time he earned the income, even though he had already assigned part of the income to his wife, and regardless of the validity of the assignment agreement under state law. The Court in Lucas v. Earl did not rule that wages are not taxable.

with respect to the following quotation:

Coppage was a criminal case involving a defendant convicted, under a Kansas statute, of firing an employee for refusing to resign as a member of a labor union. No issues of taxation were presented to or decided by the Court, and the word "tax" is not found in the text of the Court's decision.

The Truax case involved a Mr. William Truax who owned a restaurant called "English Kitchen," in Bisbee, Arizona. A Mr. Michael Corrigan and others were former cooks and waiters at the restaurant. Corrigan and others allegedly instituted a boycott of the restaurant, after a dispute arose over the terms and conditions of employment. A strike was allegedly ordered by a local union with respect to certain union members employed at the restaurant. The restaurant’s business was allegedly harmed, and Mr. Truax sued various parties on a variety of grounds. The lawsuit was thrown out by the trial court before the case could be heard, on the theory that Mr. Truax was incorrect as a matter of law. Mr. Truax appealed and the case eventually ended up in the U.S. Supreme Court. The U.S. Supreme Court ruled that the trial court should not have thrown out the lawsuit, but should have heard Mr. Truax’s case. The case was sent back to the trial court so that a trial could take place. Truax was not a tax case. No issues involving taxation were presented to or decided by the Court.

Butchers' Union Co. was a case involving interpretation of the Louisiana Constitution

and certain ordinances of the city of New Orleans. The Court ruled that the Louisiana Constitution and the New Orleans ordinances did not impermissibly impair a pre-existing obligation under a contract when those laws effectively ended a slaughter-house business monopoly by the Crescent City Company. No issues regarding the power to tax incomes from businesses, vocations, or labor were presented to or decided by the Court, and the word "tax" does not appear in the text of the decision.

Murdock (or Jones v. City of Opelika) was a case involving the validity of a city ordinance (in Jeannette, Pennsylvania) worded as follows:

A group of people who were Jehovah's Witnesses

went from door to door distributing literature in the town. They failed to obtain the license under the ordinance. The case ended up in court, and went all the way to the U.S. Supreme Court, which stated:

The protester argument appears to be that the federal government should not be able to tax income from labor because it would be a tax on an exercise of the freedoms mentioned in the quotation. The "tax" in this case was, in effect, a license fee imposed on door to door sales people under a city ordinance. The city was trying to exact the fee from Jehovah’s Witness members who were going door to door. Questions about the validity of federal income taxes were neither presented to nor decided by the Court.

The argument seems to be that because "the individual's rights to live and own property" are arguably rights against which "an excise cannot be imposed," the federal income tax on income from labor should therefore be unconstitutional. However, Redfield v. Fisher is an Oregon Supreme Court case, not a federal case. No issues involving the validity of federal income tax laws were decided by the court.

for the theory that wages are not taxable, or for the theory that dividends are not taxable. The case dealt with a stock dividend on stock that was essentially equivalent to a stock split, as opposed to a cash dividend on stock. In the case of this kind of "dividend" the stockholder does not receive anything or realize any additional value. For example, if a stockholder owns 100 shares of stock having a value of $4 per share, the total value is $400. If the corporation declares, say, a "two for one" stock dividend that is essentially similar to a stock split (and the corporation distributes no money or other property), the stockholder now has 200 shares with a value of $2 each, which is still $400 in value - i.e., no increase in value and no income. The pie is still the same size — but it's sliced into more pieces, each piece being proportionately smaller.

More directly to the point, there has been no "sale or other disposition" of the stock. The taxpayer still owns the same asset (i.e., the same interest in the corporation) he owned prior to the stock dividend. So, even if his basis amount (generally, the amount he originally paid for the stock) is less than the $400 value (i.e., even if he has an unrealized or potential gain), he still has not yet "realized" the gain. The Court ruled that this kind of stock dividend is not treated as "income" to a shareholder.

The Court in this case did not rule on any issue involving the taxability of labor or income from labor, or wages, salary or ordinary "cash" dividends — where the stockholder actually receives a check from the company, etc. Indeed, the terms "wage" and "salary" do not appear in the text of the decision in Eisner v. Macomber.

Related tax protester arguments with respect to wages paid by "employers" to "employees" are (1) that only federal officers, federal employees, elected officials, or corporate officers are "employees" for purposes of federal income tax, (2) that the inclusion of the United States government within the definition of the term "employer" operates to exclude all other employers from the definition, and (3) that with respect to compensation, the tax is imposed only on compensation paid to federal government employees. These arguments have been rejected in court rulings.

Another tax protester argument is that income from labor should not be taxable because any amount the worker receives in exchange for his or her labor is received in an exchange of "equal value," although an exchange in any true "arm's length" fair market value

transaction is, essentially by definition, an exchange of equal value. See, for example, the decision of the United States Court of Appeals for the Ninth Circuit

in United States v. Buras, in which the taxpayer's theory — that wages were not taxable because (1) "only profit or gain, such as that from the sale of a capital asset, constituted income subject to federal tax" and (2) "[w]ages could not constitute gain or profit because wages merely represent an equivalent exchange for one's labor" — was rejected. See also the decision of the United States Tax Court

in Link v. Commissioner, where the taxpayer's argument — that pension income is "labor property" and that when taxpayer receives his pension income from his former employer for whom he once performed services (or labor), any amount he receives in exchange for his labor is a nontaxable exchange of equal value — was rejected. In Boggs v. Commissioner, a penalty of $8,000 was imposed by the United States Court of Appeals for the Sixth Circuit on the taxpayers for filing a frivolous appeal using the argument that a portion of a wage amount was not taxable as a return on "human capital."

Further, under the U.S. federal tax laws, even if labor were considered "property" the gain or income from "labor property" would be defined as the excess of the amount realized (for example, the money received) by the taxpayer over the amount of the taxpayer's "adjusted basis" in the "property" (see ). Since the taxpayer can have only a zero "basis" amount in his or her own labor — the personal living expenses incurred to generate labor being both non-capitalizable and, under , non-deductible — the "gain" would thus be equal to the amount of compensation received by the taxpayer. Compare Carter v. Commissioner, where the United States Court of Appeals for the Ninth Circuit stated: "The assertion that proceeds received for personal services cannot be given a 'zero-basis for the purpose of the assessment of taxation,' is frivolous. This is a variation of the 'wages are not income' theme, which has been rejected repeatedly by this court." See also Reading v. Commissioner (taxpayer's argument — that gain from labor of self-employed individual cannot be determined until the "cost of doing labor" has been subtracted from the amount received — was rejected; validity of , disallowing deductions for personal living expenses, was upheld). See also Burnett v. Commissioner (taxpayer's argument — that wages represent an equal exchange of property and, therefore, are not taxable income — was rejected). See also In re Myrland (ruling that a taxpayer is not entitled to deduct the value of his labor from his income in calculating his taxes).

in Cheek v. United States

, the United States Supreme Court specifically labeled defendant John Cheek's arguments about the constitutionality of the tax law — arguments Cheek had raised in various prior court cases — as "frivolous." Prior to his conviction, John Cheek had specifically contended that the Sixteenth Amendment did not authorize a tax on wages and salaries, but only on gain or profit.

Income tax in the United States

In the United States, a tax is imposed on income by the Federal, most states, and many local governments. The income tax is determined by applying a tax rate, which may increase as income increases, to taxable income as defined. Individuals and corporations are directly taxable, and estates and...

violates the United States Constitution

United States Constitution

The Constitution of the United States is the supreme law of the United States of America. It is the framework for the organization of the United States government and for the relationship of the federal government with the states, citizens, and all people within the United States.The first three...

. These kinds of tax protester arguments

Tax protester arguments

Tax protester arguments are a number of objections raised by individuals who deny that a person has a legal obligation to pay a tax for which the United States government has determined that person is liable....

are distinguished from related statutory arguments

Tax protester statutory arguments

Tax protesters in the United States make a number of statutory arguments that the assessment of the federal income tax in the United States violates the statutes enacted by the United States Congress and signed into law by the President...

and conspiracy arguments

Tax protester conspiracy arguments

Tax protester conspiracy arguments are arguments raised by tax protesters who assert that the imposition of the federal income tax in the United States is the result of an illicit conspiracy. These kinds of arguments are distinguished from related constitutional arguments and statutory arguments...

, which presuppose the constitutionality of the income tax. Although the most frequent Constitutional arguments are directed towards the validity and effect of the Sixteenth Amendment

Tax protester Sixteenth Amendment arguments

Tax protester Sixteenth Amendment arguments are assertions that the imposition of the U.S. federal income tax is illegal because the Sixteenth Amendment to the United States Constitution, which reads "The Congress shall have power to lay and collect taxes on incomes, from whatever source derived,...

, arguments exist that the income tax violates some other provision of the Constitution; or that some other provision, that would prevent the assessment of the income tax, was ratified but wrongfully excluded from the Constitution.

Other constitutional amendment arguments have been raised by tax protesters. Some argue that imposition of the income tax violates the First Amendment

First Amendment to the United States Constitution

The First Amendment to the United States Constitution is part of the Bill of Rights. The amendment prohibits the making of any law respecting an establishment of religion, impeding the free exercise of religion, abridging the freedom of speech, infringing on the freedom of the press, interfering...

freedom of speech

Freedom of speech

Freedom of speech is the freedom to speak freely without censorship. The term freedom of expression is sometimes used synonymously, but includes any act of seeking, receiving and imparting information or ideas, regardless of the medium used...

and freedom of religion

Freedom of religion

Freedom of religion is a principle that supports the freedom of an individual or community, in public or private, to manifest religion or belief in teaching, practice, worship, and observance; the concept is generally recognized also to include the freedom to change religion or not to follow any...

. Protesters argue that the income tax violates the Fifth Amendment

Fifth Amendment to the United States Constitution

The Fifth Amendment to the United States Constitution, which is part of the Bill of Rights, protects against abuse of government authority in a legal procedure. Its guarantees stem from English common law which traces back to the Magna Carta in 1215...

right against self-incrimination

Self-incrimination

Self-incrimination is the act of accusing oneself of a crime for which a person can then be prosecuted. Self-incrimination can occur either directly or indirectly: directly, by means of interrogation where information of a self-incriminatory nature is disclosed; indirectly, when information of a...

, the Takings Clause, or the right that no person shall be "deprived of life, liberty, or property, without due process of law". Tax protesters have argued that income taxes impose involuntary servitude

Involuntary servitude

Involuntary servitude is a United States legal and constitutional term for a person laboring against that person's will to benefit another, under some form of coercion other than the worker's financial needs...

in violation of the Thirteenth Amendment

Thirteenth Amendment to the United States Constitution

The Thirteenth Amendment to the United States Constitution officially abolished and continues to prohibit slavery and involuntary servitude, except as punishment for a crime. It was passed by the Senate on April 8, 1864, passed by the House on January 31, 1865, and adopted on December 6, 1865. On...

. Some tax protesters argue that Americans are citizens of the individual states as opposed to citizens of the United States, as the Fourteenth Amendment

Fourteenth Amendment to the United States Constitution

The Fourteenth Amendment to the United States Constitution was adopted on July 9, 1868, as one of the Reconstruction Amendments.Its Citizenship Clause provides a broad definition of citizenship that overruled the Dred Scott v...

was not properly ratified. Another argument is a missing amendment to the Constitution, known as the Titles of Nobility Amendment

Titles of Nobility amendment

The Titles of Nobility Amendment was proposed as an amendment to the United States Constitution in 1810. Upon approval of a resolution offered by U.S. Senator Philip Reed of Maryland, during the 2nd Session of the 11th Congress, TONA was submitted to the state legislatures for ratification...

, which precedes the current Thirteenth Amendment. Another argument raised is that because the federal income tax is progressive

Progressive tax

A progressive tax is a tax by which the tax rate increases as the taxable base amount increases. "Progressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from low to high, where the average tax rate is less than the marginal tax rate...

, the discriminations and inequalities created by the tax should render the tax unconstitutional. These arguments have been rejected by the courts.

The authority of the federal government has been challenged by protesters, arguing that they should be immune from federal income taxation because they are sovereign individuals or natural individuals, have not requested a privilege or benefit from the government, or are outside the "federal zone" (D.C.

Washington, D.C.

Washington, D.C., formally the District of Columbia and commonly referred to as Washington, "the District", or simply D.C., is the capital of the United States. On July 16, 1790, the United States Congress approved the creation of a permanent national capital as permitted by the U.S. Constitution....

and various federal enclaves such as military bases). Neither the U.S. Supreme Court nor any other federal court has ruled that an income tax imposed under the Internal Revenue Code

Internal Revenue Code

The Internal Revenue Code is the domestic portion of Federal statutory tax law in the United States, published in various volumes of the United States Statutes at Large, and separately as Title 26 of the United States Code...

of 1986 is unconstitutional. Under the Supreme Court ruling in Cheek v. United States

Cheek v. United States

In Cheek v. United States, 498 U.S. 192 , the United States Supreme Court reversed the conviction of John L. Cheek, a tax protester, for willful failure to file tax returns and pay tax...

, a defendant in a tax evasion

Tax evasion

Tax evasion is the general term for efforts by individuals, corporations, trusts and other entities to evade taxes by illegal means. Tax evasion usually entails taxpayers deliberately misrepresenting or concealing the true state of their affairs to the tax authorities to reduce their tax liability,...

prosecution who has made arguments that the federal income tax laws are unconstitutional may have the arguments turned against him (or her). Such arguments, even if based on honestly held beliefs, may constitute evidence that helps the prosecutor prove willfulness, one of the elements of tax evasion.

First Amendment

Some protesters argue that imposition of income taxes violates the First AmendmentFirst Amendment to the United States Constitution

The First Amendment to the United States Constitution is part of the Bill of Rights. The amendment prohibits the making of any law respecting an establishment of religion, impeding the free exercise of religion, abridging the freedom of speech, infringing on the freedom of the press, interfering...

freedom of speech

Freedom of speech

Freedom of speech is the freedom to speak freely without censorship. The term freedom of expression is sometimes used synonymously, but includes any act of seeking, receiving and imparting information or ideas, regardless of the medium used...

because it requires the subject of the tax to write information on a tax return; or violates freedom of religion

Freedom of religion

Freedom of religion is a principle that supports the freedom of an individual or community, in public or private, to manifest religion or belief in teaching, practice, worship, and observance; the concept is generally recognized also to include the freedom to change religion or not to follow any...

if the subject of the tax claims some religious objection to the payment of taxes, particularly if the subject styles himself or herself as a Reverend, Minister, or other religious office-holder. While the Internal Revenue Code

Internal Revenue Code

The Internal Revenue Code is the domestic portion of Federal statutory tax law in the United States, published in various volumes of the United States Statutes at Large, and separately as Title 26 of the United States Code...

makes an exemption for churches and other religious institutions, it makes only special tax codes and deductions, not exceptions, for religious professionals. The United States Supreme Court held in 1878 Reynolds v. United States

Reynolds v. United States

Reynolds v. United States, , was a Supreme Court of the United States case that held that religious duty was not a suitable defense to a criminal indictment...

, that a religious belief, however strongly held, does not exempt the believer from adhering to general laws.

Self incrimination

Fifth Amendment to the United States Constitution

The Fifth Amendment to the United States Constitution, which is part of the Bill of Rights, protects against abuse of government authority in a legal procedure. Its guarantees stem from English common law which traces back to the Magna Carta in 1215...

right against self-incrimination allows an individual to refuse to file an income tax return calling for information that could lead to a conviction for criminal acts from which the income was derived, or for the crime of not paying the tax itself. In response, the courts generally refer to the case of United States v. Sullivan, where Justice Oliver Wendell Holmes

Oliver Wendell Holmes, Jr.

Oliver Wendell Holmes, Jr. was an American jurist who served as an Associate Justice of the Supreme Court of the United States from 1902 to 1932...

wrote:

Takings Clause

Some protesters have argued that the income tax is a prohibited "takings" under the Fifth Amendment's Takings Clause, and can not be imposed unless the taxpayer receives just compensation. The United States Supreme Court rejected this argument in Brushaber v. Union Pacific RailroadBrushaber v. Union Pacific Railroad

Brushaber v. Union Pacific Railroad, 240 U.S. 1 , was a landmark United States Supreme Court case in which the Court upheld the validity of a tax statute called the Revenue Act of 1913, also known as the Tariff Act, Ch. 16, 38 Stat. 166 Brushaber v. Union Pacific Railroad, 240 U.S. 1 (1916), was a...

. The takings argument and variations of this argument have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

Other arguments

Protesters argue that the income tax violates the Fifth Amendment right that no person shall be "deprived of life, liberty, or property, without due process of law". However, people can be deprived of life, liberty, or property with due process of law — this is what the courts do. Legal commentator Daniel B. Evans describes:Fifth Amendment "due process" arguments by tax protesters were rejected by the United States Court of Appeals for the Third Circuit in Kahn v. United States, by the United States Court of Appeals for the Fifth Circuit in Anderson v. United States, by the United States Court of Appeals for the Seventh Circuit in Cameron v. Internal Revenue Serv., by the United States Court of Appeals for the Eighth Circuit in Baskin v. United States, by the United States Court of Appeals for the Ninth Circuit in Jolly v. United States, and by the United States Court of Appeals for the Tenth Circuit in Martinez v. Internal Revenue Serv.

Thirteenth Amendment

An early protester, Arthur J. Porth, argued that the Sixteenth Amendment to the U.S. Constitution should itself be declared unconstitutional. His theory was that the income taxes under the Internal Revenue Code of 1939 imposed "involuntary servitudeInvoluntary servitude

Involuntary servitude is a United States legal and constitutional term for a person laboring against that person's will to benefit another, under some form of coercion other than the worker's financial needs...

" in violation of the Thirteenth Amendment

Thirteenth Amendment to the United States Constitution

The Thirteenth Amendment to the United States Constitution officially abolished and continues to prohibit slavery and involuntary servitude, except as punishment for a crime. It was passed by the Senate on April 8, 1864, passed by the House on January 31, 1865, and adopted on December 6, 1865. On...

. That argument was ruled to be without merit in Porth v. Brodrick, United States Collector of Internal Revenue for the State of Kansas. The involuntary servitude argument, and variations of this argument, have been officially identified as legally frivolous

Frivolous or vexatious

In the law of several jurisdictions, such as Ireland and New Zealand, frivolous or vexatious, when used to describe an action such as a complaint or a legal proceeding, is a term used to deny its being heard, or to dismiss or strike out any ensuing judicial or non-judicial processes.While the term...

federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

Fourteenth Amendment

Some tax protesters argue that all Americans are citizens of individual states as opposed to citizens of the United States, and that the United States therefore has no power to tax citizens or impose other federal laws outside of Washington D.C. and other federal enclaves The first sentence of Section 1 of the Fourteenth AmendmentFourteenth Amendment to the United States Constitution

The Fourteenth Amendment to the United States Constitution was adopted on July 9, 1868, as one of the Reconstruction Amendments.Its Citizenship Clause provides a broad definition of citizenship that overruled the Dred Scott v...

states:

Notably, some tax protesters contend that the Fourteenth Amendment itself was never properly ratified, under the theory that the governments of southern states that supported the post-Civil War amendments were not representative of the people.

Courts have uniformly held that this argument that the Fourteenth Amendment divested state citizens of U.S. citizenship is plainly incorrect. In Kantor v. Wellesley Galleries, Ltd., the court explained that "[w]hile the Fourteenth Amendment does not create a national citizenship, it has the effect of making that citizenship 'paramount and dominant' instead of 'derivative and dependent' upon state citizenship". See also United States v. Ward,Fox v. Commissioner, and United States v. Baker.

Seventeenth Amendment

An argument raised in the case of Trohimovich v. Commissioner is that the Seventeenth Amendment to the United States ConstitutionSeventeenth Amendment to the United States Constitution

The Seventeenth Amendment to the United States Constitution established direct election of United States Senators by popular vote. The amendment supersedes Article I, § 3, Clauses 1 and 2 of the Constitution, under which senators were elected by state legislatures...

was not propertly ratified, and that all laws passed by Congress since the year 1919 (which was not the year of ratification) are invalid. The Trohimovich case involved a criminal contempt charge against the taxpayer in connection with a failure to obey a subpoena to produce books and records needed for the trial of the case. The United States Tax Court stated:

The court rejected the taxpayer's arguments, and ordered that "he be imprisoned for 30 days as punishment" for criminal contempt in failing to obey court orders or subpoenas.

Titles of Nobility Amendment

Another tax protester argument is that a 'missing' Thirteenth Amendment to the Constitution known as the Titles of Nobility AmendmentTitles of Nobility amendment

The Titles of Nobility Amendment was proposed as an amendment to the United States Constitution in 1810. Upon approval of a resolution offered by U.S. Senator Philip Reed of Maryland, during the 2nd Session of the 11th Congress, TONA was submitted to the state legislatures for ratification...

or "TONA" precedes the current Thirteenth Amendment

Thirteenth Amendment to the United States Constitution

The Thirteenth Amendment to the United States Constitution officially abolished and continues to prohibit slavery and involuntary servitude, except as punishment for a crime. It was passed by the Senate on April 8, 1864, passed by the House on January 31, 1865, and adopted on December 6, 1865. On...

; the missing amendment purportedly would have divested the citizenship of any person receiving a title of nobility. Therefore, actions taken by lawyers and judges, who use the title 'Esquire

Esquire

Esquire is a term of West European origin . Depending on the country, the term has different meanings...

' (which some protesters claim is a title of nobility), are monarchical, and therefore unconstitutional. This contention, rarely raised before courts, was most recently addressed in Campion v. Towns, No.CV-04-1516PHX-ROS, *2 n.1

Case citation

Case citation is the system used in many countries to identify the decisions in past court cases, either in special series of books called reporters or law reports, or in a 'neutral' form which will identify a decision wherever it was reported...

(D. Ariz. 2005) as a defense to a charge of tax evasion. The court replied:

Federal government authority

Sovereign individual, government privilege, and similar arguments

Some tax protesters argue that they should be immune from federal income taxation because they are sovereign individualSelf-ownership

Self-ownership is the concept of property in one's own person, expressed as the moral or natural right of a person to be the exclusive controller of his own body and life. According to G...

s or "natural individuals," or on the ground that they have not requested a privilege or benefit from the government. These kinds of arguments have been ruled without merit. For example, in the case of Lovell v. United States the United States Court of Appeals for the Seventh Circuit stated:

The Court of Appeals in Lovell affirmed a U.S. District Court order upholding a frivolous return penalty under . Similarly, in United States v. Sloan, the taxpayer's contention — that he is "not a citizen of the United States, but rather, that he is a freeborn, natural individual, a citizen of the State of Indiana, and a 'master'—not 'servant'—of his government" — was ruled to be not a legal ground for the argument that the taxpayer was not subject to the federal tax laws; the tax evasion conviction was upheld by the United States Court of Appeals for the Seventh Circuit. Similarly, the United States Court of Appeals for the Third Circuit stated, in Powers v. Commissioner: "Powers [the taxpayer] contends that either he is immune from the tax laws, or he is a 'slave' to the federal government. This false choice is a creature of Powers' tax protester ideology, not the laws of this Republic." Similarly, in 2008 the United States Court of Appeals for the Tenth Circuit rejected a taxpayer's argument that gains of an individual's labor could be taxed only if the gains were received from a "federal venue". In that case, the taxpayer's argument -- that the IRS had no ability to impose a tax on the taxpayer because he was a citizen "of the several states," but not a "federal U.S. citizen" -- was ruled to be frivolous.

Variations of the argument that an individual is a “sovereign” have been rejected in tax cases such as United States v. Hart, Risner v. Commissioner, Maxwell v. Snow, Rowe v. Internal Revenue Serv., Cobin v. Commissioner, and Glavin v. United States.

The argument that an individual who received Form W-2 wages or other compensation is not subject to federal income tax because the individual has "neither requested, obtained, nor exercised any privilege from an agency of government" was ruled frivolous by the United States Court of Appeals for the First Circuit in Sullivan v. United States and again in Kelly v. United States. See also United States v. Buras (argument that the taxpayer can be subject to an excise tax only if he benefits from a "privilege extended by a government agency" was rejected).

The argument that an individual who received Form W-2 wages is not subject to federal income tax unless the tax is imposed in connection with "government granted privileges" was ruled frivolous by the United States Court of Appeals for the Seventh Circuit in Coleman v. Commissioner. The argument that an individual who received Form W-2 wages is not subject to federal income tax unless the taxpayer enjoys a "grant of privilege or franchise" was ruled frivolous by the United States Court of Appeals for the Eighth Circuit in May v. Commissioner. The argument that an individual who received Form W-2 wages is not subject to federal income tax unless the taxpayer has obtained a "privilege from a governmental agency" was ruled frivolous by the United States Court of Appeals for the Ninth Circuit in Olson v. United States, and by the United States Court of Appeals for the Tenth Circuit in Prout v. United States.

In the case of Steward Machine Company v. Davis

Steward Machine Company v. Davis

Steward Machine Company v. Davis, 301 U.S. 548 , was a case in which the Supreme Court of the United States upheld the unemployment compensation provisions of the Social Security Act of 1935. The Act established a national taxing structure designed to induce states to adopt laws for funding and...

, the Supreme Court rejected the argument that "the relation of employment is one so essential to the pursuit of happiness that it may not be burdened with a tax," and upheld the validity of the Social Security tax. The Court stated: ". . . natural rights, so called, are as much subject to taxation as rights of less importance. An excise is not limited to vocations or activities that may be prohibited altogether. It is not limited to those that are the outcome of a franchise. It extends to vocations or activities pursued as of common right.".

Regarding the taxability of income in connection with events or activities not involving a government privilege or franchise, the United States Supreme Court stated in United States v. Sullivan that gains from illegal traffic in liquor are subject to the Federal income tax. The U.S. Supreme Court ruled in Rutkin v. United States that the receipt of money obtained by extortion is taxable as income to the wrongdoer.. The U.S. Supreme Court ruled in James v. United States that the receipt of money obtained through embezzlement is taxable as income to the wrongdoer, even though the wrongdoer is required to return the money to its owner.

The argument that a person's income is not taxed when the person rejects or renounces United States citizenship because the person claims to be a citizen exclusively of a state, and variations of this argument, have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

Federal zone

Some tax protesters argue that under article I, section 8, clause 17 of the U.S. Constitution, federal income taxes can be imposed only inside an area called the "federal zone" — limited to the District of Columbia and various federal enclaves such as military bases. Clause 17 provides that Congress shall have the power:This argument is based in part on the U.S. Supreme Court decision in the case of United States v. Bevans. In Bevans, the parties argued over whether a federal court in Massachusetts had jurisdiction over the case of a U.S. Marine charged with a murder that occurred on a ship in Boston Harbor. No issues regarding federal income taxation or the Internal Revenue Code were presented to or decided by the Court in the Bevans case. The Internal Revenue Code and the Internal Revenue Service did not yet exist in 1818, when the Bevans murder case was decided.

The Clause 17 argument was specifically rejected in the case of United States v. Sato:

The Clause 17 argument was also unsuccessful in Celauro v. United States, Internal Revenue Service.

Some tax protesters contend that the U.S. Supreme Court decision in Caha v. United States restricts the jurisdiction of the federal government to impose income taxes inside the "states", based on the following language from the Court’s opinion:

Some tax protesters contend that the Court's reference to "those matters" restricted the federal government's jurisdiction over matters of taxation. Caha is not a tax case. The reference to "this statute" was a reference to a perjury statute. The Caha case involved a perjury conviction where the defendant unsuccessfully argued that the federal court had no jurisdiction over a prosecution for the crime of perjury committed in a proceeding in a land office at Kingfisher, Oklahoma regarding ownership of real estate.

The reference in Caha to the "laws of congress in respect to those matters" was a reference to the matters of preservation of the peace and the protection of person and property. The Court in Caha rejected the argument that the federal courts had no jurisdiction to hear a case under the perjury statute, and the defendant's conviction was affirmed. No issues involving the power to impose and enforce federal taxes in the fifty states were presented to or decided by the court in Caha.

The courts have uniformly rejected the "federal zone" argument that congressional authority to impose an income tax is limited to the District of Columbia, forts, magazines, arsenals, or dockyards, etc. See, for example, United States v. Mundt; Nelsen v. Commissioner; Abbs v. Imhoff.

Stratton's Independence, Limited v. Howbert

Some tax protesters have cited the U.S. Supreme Court case of Stratton's Independence, Limited v. Howbert for the argument that an income tax on an individual's income is unconstitutional. This was an argument raised unsuccessfully by John B. Hill, Jr., in Hill v. United States. and without success by John B. Cameron, Jr., in Cameron v. Internal Revenue Serv.. In Stratton, a mining corporation argued that the 1909 corporation tax act did not apply to that corporation. The U.S. Supreme Court ruled that the 1909 corporation tax act did apply to mining corporations, and that the proceeds of ores mined by the corporation from its own premises were income within the meaning of the 1909 tax act. The Court also ruled that the corporation was not entitled to deduct "the value of such ore in place and before it is mined" as depreciation within the meaning of the 1909 Act. The Stratton case involved income taxation of a corporation, not of individuals. The Court in the Stratton case did not rule any corporate or individual income tax as unconstitutional.Doyle v. Mitchell Bros. Co.

Some tax protesters have cited Doyle v. Mitchell Bros. Co. for the proposition that income of individuals cannot be taxed. This was the argument raised unsuccessfully by Joseph T. Tornichio in the case of Tornichio v. United States and by Joram Perl in Perl v. United States (also unsuccessfully). The following language is sometimes cited by protesters:The above verbiage is immediately followed in the text of the case by this sentence:

In Doyle, the taxpayer was a corporation engaged in the manufacture of lumber. In 1903, the taxpayer purchased certain timber land at a cost of about 20 $/acre. As of December 31, 1908, the value of the land had increased to about 40 $/acre. The Corporation Excise Tax Act of 1909 was enacted on August 5, 1909, and was effective retroactively to January 1, 1909. For the years 1909 through 1912, the taxpayer filed tax returns under the 1909 Act, showing gross receipts from the sale of manufactured lumber and, in arriving at the amount of net income subject to tax under the 1909 Act, deducted an amount based on the $40-per-acre value, rather than the actual cost of about $20 per acre. The Commissioner of Internal Revenue argued that the taxpayer should be able to deduct only an amount based on the taxpayer’s historical cost basis of $20, rather than the $40 fair market value at the time the 1909 Act became effective. (Essentially, if the taxpayer were allowed to use the $40 per acre value as its basis rather than the actual $20 historical cost basis, a portion of the taxpayer’s gain — the increase in value from 1903 to December 31, 1908 — would go untaxed.)

The U.S. Supreme Court ruled that under the 1909 Act — which had become effective January 1, 1909 — the taxpayer should be taxed only on the increase in value after 1908. Increases in value prior to the effective date of the statute were not to be taxed under the terms of that statute. Thus, the taxpayer was entitled to deduct, from its gross receipts from the sale of finished lumber, a basis amount computed with reference to the $40 per acre value as of December 31, 1908. Doyle is a case involving statutory (not constitutional) interpretation. In this case, the Court was interpreting the 1909 statute. Although some tax protesters cite this case for an argument about the constitutional definition of income as excluding income of individuals, no issues involving the constitutional definition of income, or of income under any other tax statutes, were presented to or decided by the Court.

The case is also notable for the fact that it involved a retroactively imposed tax. The taxpayer did not argue — and the Court did not rule — that as a general proposition taxes could not be imposed retroactively. Indeed, the tax in this case was imposed retroactively; the statute was enacted in August 1909 but was made effective retroactively to January 1, 1909.

Corporate profits

One argument repeatedly made by tax protesters is that the income of individuals is not taxable because income should mean only "corporate profits" or "corporate gain". This is the Merchants' Loan argument, named after the case of Merchants’ Loan & Trust Company, as Trustee of the Estate of Arthur Ryerson, Deceased, Plaintiff in Error v. Julius F. Smietanka, formerly United States Collector of Internal Revenue for the First District of the State of Illinois. The argument is essentially that "income" for federal income tax purposes means only the income of a corporation — not the income of a non-corporate taxpayer — because the United States Supreme Court in that case, in discussing the meaning of income, mentioned a statute enacted in 1909 that taxed the income of corporations.The Court in Merchants' Loan was specifically interpreting a 1916 statute imposing income taxes on individuals and estates (among other kinds of entities), and not the 1909 corporate tax statute. The taxpayer in Merchants' Loan was not a corporation but was the "Estate of Arthur Ryerson, Deceased". The Court was not presented with (and did not decide) any issue involving the taxability of "corporate profits" or "corporate gains" or any other kind of income except the gain on the sale of the stock by the "Estate of Arthur Ryerson, Deceased". The terms "corporate profit" and "corporate gain" are not found in the text of the Court’s decision in Merchants’ Loan. In Merchants' Loan, the Supreme Court ruled that under the Sixteenth Amendment to the United States Constitution and the 1916 tax statute applicable at the time, a gain on a sale of stock by the estate of a deceased person is included in the income of that estate, and is therefore taxable to that estate for federal income tax purposes.

The Merchants' Loan argument has been litigated by tax protesters several times, and the courts have uniformly rejected the argument that income consists only of corporate profits. See, for example: Cameron v. Internal Revenue Serv., Stoewer v. Commissioner, Reinhart v. United States, Fink v. Commissioner; Flathers v. Commissioner; Schroeder v. Commissioner; Sherwood v. Commissioner; and Ho v. Commissioner. Tax protesters — who have lost every case using Merchants' Loan for the theory that only "corporate profits" could be taxable — are citing a case where the U.S. Supreme Court ruled that the income of a non-corporate taxpayer is taxable. Neither the United States Supreme Court nor any other federal court has ever ruled that under the Internal Revenue Code the term "income" means only the income of a corporation for federal income tax purposes.

Some tax protesters have cited the Supreme Court case of Flint v. Stone Tracy Co.

Flint v. Stone Tracy Co.

Flint v. Stone Tracy Co. 220 U.S. 107 was a United States Supreme Court case challenging the validity of an income tax on corporations...

for the argument that only corporate profits or income can be taxed, using the following quotation:

In Flint v. Stone Tracy Co., the U.S. Supreme Court ruled that the corporation tax act of 1909 did not violate the constitutional requirement that revenue measures originate in the U.S. House of Representatives. The Court did not rule that excise taxes consisted only of taxes on corporations and corporate privileges, to the exclusion of taxes on individuals (natural persons). The issue of the validity of an income tax imposed on individuals was neither presented to the Court nor decided by the Court.

The courts have rejected the argument that Flint v. Stone Tracy Co. can be used to avoid taxation of wages. For example, in Parker v. Commissioner, a case where a taxpayer unsuccessfully argued that wages were not taxable, the United States Court of Appeals for the Fifth Circuit stated (in part):

The argument that only corporations are subject to federal income tax, and variations of this argument, have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

Cases indicating definition of income is irrelevant

At least two federal courts have indicated that Congress may constitutionally tax an item as "income," regardless of whether that item is "income" within the meaning of the Sixteenth Amendment. In Penn Mutual Indemnity Co. v. Commissioner, the United States Court of Appeals for the Third Circuit stated:In Murphy v. Internal Revenue Serv.

Murphy v. IRS

Marrita Murphy and Daniel J. Leveille, Appellants v. Internal Revenue Service and United States of America, Appellees , is a controversial tax case in which the United States Court of Appeals for the District of Columbia Circuit originally held that the taxation of emotional distress awards by the...

, the United States Court of Appeals for the District of Columbia Circuit ruled that a personal injury award received by a taxpayer was "within the reach of the congressional power to tax under Article I, Section 8 of the Constitution" — even if the award was "not income within the meaning of the Sixteenth Amendment".

Progressive taxation

One argument that has been raised is that because the federal income tax is progressiveProgressive tax

A progressive tax is a tax by which the tax rate increases as the taxable base amount increases. "Progressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from low to high, where the average tax rate is less than the marginal tax rate...

(i.e., because the marginal tax rates increase, or progress, as the level of taxable income increases), the discriminations and inequalities created by the tax should render the tax unconstitutional. This argument was rejected by the United States Supreme Court in two companion cases — with respect to the income tax on individuals in Thorne v. Anderson, and with respect to the income tax on corporations in Tyee Realty Co. v. Anderson.

Taxing labor or income from labor

Several tax protesters assert that the Congress has no constitutional power to tax labor or income from labor, citing a variety of court cases. These arguments include claims that the word "incomeIncome

Income is the consumption and savings opportunity gained by an entity within a specified time frame, which is generally expressed in monetary terms. However, for households and individuals, "income is the sum of all the wages, salaries, profits, interests payments, rents and other forms of earnings...

" as used in the Sixteenth Amendment cannot be interpreted as applying to wage

Wage

A wage is a compensation, usually financial, received by workers in exchange for their labor.Compensation in terms of wages is given to workers and compensation in terms of salary is given to employees...

s; that wages are not income

Income

Income is the consumption and savings opportunity gained by an entity within a specified time frame, which is generally expressed in monetary terms. However, for households and individuals, "income is the sum of all the wages, salaries, profits, interests payments, rents and other forms of earnings...

because labor is exchanged for them; that taxing wages violates individuals' right to property; and several others.

Another protester argument is that the U.S. Constitution authorizes the income tax only on income derived from activities that are government-licensed or otherwise specially protected. The courts have rejected this theory, ruling that "Congress has taxed compensation for services, without any regard for whether that compensation is derived from government-licensed or specially protected activities, [ . . . ] and this has been construed to cover earnings from labor."

Robert L. Schulz and his We the People Foundation

We the People Foundation

We the People Foundation for Constitutional Education, Inc. also known as We the People Foundation is a non-profit education and research organization in Queensbury, New York with the declared mission "to protect and defend individual Rights as guaranteed by the Constitutions of the United States."...

take the positions that the government "is clearly prohibited from doing what it is doing – taxing the salaries, wages and compensation of the working men and women of this country and forcing the business entities that utilize the labor of ordinary American citizens to withhold and turn over to the IRS a part of the earnings of those workers" and "that the federal government DOES NOT possess ANY legal authority -- statutory or Constitutional -- to tax the wages or salaries of American workers."

Similarly, tax protester Tom Cryer

Tom Cryer

Tommy K. Cryer, also known as Tom Cryer , is an attorney in Shreveport, Louisiana who was charged with and later acquitted of willful failure to file U.S. Federal income tax returns in a timely fashion. In a pending case in United States Tax Court, Cryer is contesting a determination by the U.S...