Leveraged buyout

Encyclopedia

A leveraged buyout occurs when an investor, typically financial sponsor

, acquires a controlling interest

in a company's equity

and where a significant percentage of the purchase price is financed through leverage

(borrowing

). The assets of the acquired company are used as collateral for the borrowed capital, sometimes with assets of the acquiring company. Typically, leveraged buyout uses a combination of various debt instruments from bank and debt capital markets. The bonds or other paper issued for leveraged buyouts are commonly considered not to be investment grade because of the significant risks involved. If the company subsequently defaults on its debts, the LBO transaction will frequently be challenged by creditors or a bankruptcy trustee under a theory of fraudulent transfer

Companies of all sizes and industries have been the target of leveraged buyout transactions, although because of the importance of debt and the ability of the acquired firm to make regular loan payments after the completion of a leveraged buyout, some features of potential target firms make for more attractive leverage buyout candidates, including:

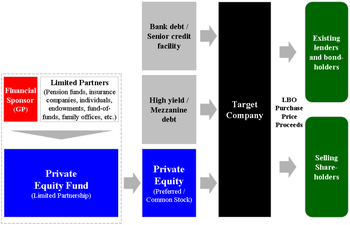

Leveraged buyouts involve institutional investors and financial sponsor

Leveraged buyouts involve institutional investors and financial sponsor

s (like a private equity firm

) making large acquisitions without committing all the capital required for the acquisition. To do this, a financial sponsor will raise acquisition debt (by issuing bonds or securing a loan) which is ultimately secured upon the acquisition target and also looks to the cash flows of the acquisition target to make interest and principal payments. Acquisition debt in an LBO is therefore usually non-recourse

to the financial sponsor and to the equity fund that the financial sponsor manages. Furthermore, unlike in a hedge fund, where debt raised to purchase certain securities is also collateralized by the fund's other securities, the acquisition debt in an LBO is recourse only to the company purchased in a particular LBO transaction. Therefore, an LBO transaction's financial structure is particularly attractive to a fund's limited partners, allowing them the benefits of leverage but greatly limiting the degree of recourse of that leverage.

This kind of acquisition brings leverage benefits to an LBO's financial sponsor in two ways: (1) the investor itself only needs to provide a fraction of the capital for the acquisition, and (2) assuming the economic internal rate of return on the investment (taking into account expected exit proceeds) exceeds the weighted average interest rate on the acquisition debt, returns to the financial sponsor will be significantly enhanced.

As transaction sizes grow, the equity component of the purchase price can be provided by multiple financial sponsors "co-investing" to come up with the needed equity for a purchase. Likewise, multiple lenders may band together in a "syndicate" to jointly provide the debt required to fund the transaction. Today, larger transactions are dominated by dedicated private equity

firms and a limited number of large banks with "financial sponsors" groups.

As a percentage of the purchase price for a leverage buyout target, the amount of debt used to finance a transaction varies according to the financial condition and history of the acquisition target, market conditions, the willingness of lenders

to extend credit (both to the LBO's financial sponsor

s and the company to be acquired) as well as the interest costs and the ability of the company to cover those costs. Typically the debt portion of a LBO ranges from 50%-85% of the purchase price, but in some cases debt may represent upwards of 95% of purchase price. Between 2000-2005 debt averaged between 59.4% and 67.9% of total purchase price for LBOs in the United States.

To finance LBO's, private-equity firms usually issue some combination of syndicated loan

s and high-yield bonds. Smaller transactions may also be financed with mezzanine debt from insurance companies or specialty lenders. Syndicated loans are typically arranged by investment banks and financed by commercial banks and loan fund managers, such as mutual funds, hedge funds, credit opportunity investors and structured finance vehicles. The commercial banks typically provide revolving credit

s that provide issuers with liquidity and cash flow while fund managers generally provided funded term loans that are used to finance the LBO. These loans tend to be senior secured, floating-rate instruments pegged to the London Interbank Offered Rate

(LIBOR). They are typically pre-payable at the option of the issuer, though in some cases modest prepayment fees apply. High-yield bonds, meanwhile, are also underwritten by investment banks but are financed by a combination of retail and institutional credit investors, including high-yield mutual funds, hedge funds, credit opportunities and other institutional accounts. High-yield bonds tend to be fixed-rate instruments. Most are unsecured, though in some cases issuers will sell senior secured notes. The bonds usually have no-call periods of 3–5 years and then high prepayment fees thereafter. Issuers, however, will in many cases have a "claw-back option" that allows them to repay some percentage during the no-call period (usually 35%) with equity proceeds.

Another source of financing for LBO's is seller's notes, which are provided in some cases by the entity as a way to facilitate the transaction.

in May 1955. Under the terms of that transaction, McLean borrowed $42 million and raised an additional $7 million through an issue of preferred stock

. When the deal closed, $20 million of Waterman cash and assets were used to retire $20 million of the loan debt.

Similar to the approach employed in the McLean transaction, the use of publicly traded holding companies as investment vehicles to acquire portfolios of investments in corporate assets was a relatively new trend in the 1960s, popularized by the likes of Warren Buffett

(Berkshire Hathaway

) and Victor Posner

(DWG Corporation), and later adopted by Nelson Peltz

(Triarc), Saul Steinberg

(Reliance Insurance) and Gerry Schwartz

(Onex Corporation). These investment vehicles would utilize a number of the same tactics and target the same type of companies as more traditional leveraged buyouts and in many ways could be considered a forerunner of the later private equity firms. In fact it is Posner who is often credited with coining the term "leveraged buyout" or "LBO"

The leveraged buyout boom of the 1980s was conceived by a number of corporate financiers, most notably Jerome Kohlberg, Jr.

and later his protégé Henry Kravis

. Working for Bear Stearns

at the time, Kohlberg and Kravis, along with Kravis' cousin George Roberts

, began a series of what they described as "bootstrap" investments. Many of the target companies lacked a viable or attractive exit for their founders, as they were too small to be taken public and the founders were reluctant to sell out to competitors. Thus a sale to a financial buyer

might prove attractive. Their acquisition of Orkin Exterminating Company

in 1964 is among the first significant leveraged buyout transactions.. In the following years the three Bear Stearns

bankers would complete a series of buyouts including Stern Metals (1965), Incom (a division of Rockwood International, 1971), Cobblers Industries (1971), and Boren Clay (1973) as well as Thompson Wire, Eagle Motors and Barrows through their investment in Stern Metals. By 1976, tensions had built up between Bear Stearns and Kohlberg, Kravis and Roberts leading to their departure and the formation of Kohlberg Kravis Roberts in that year.

During the 1980s, constituencies within acquired companies and the media ascribed the "corporate raid

" label to many private equity investments, particularly those that featured a hostile takeover of the company, perceived asset stripping

, major layoffs or other significant corporate restructuring activities. Among the most notable investors to be labeled corporate raiders in the 1980s included Carl Icahn

, Victor Posner

, Nelson Peltz

, Robert M. Bass

, T. Boone Pickens, Harold Clark Simmons

, Kirk Kerkorian

, Sir James Goldsmith, Saul Steinberg

and Asher Edelman

. Carl Icahn

developed a reputation as a ruthless corporate raider after his hostile takeover of TWA

in 1985. Many of the corporate raiders were onetime clients of Michael Milken

, whose investment banking firm, Drexel Burnham Lambert

helped raise blind pools of capital with which corporate raiders could make a legitimate attempt to take over a company and provided high-yield debt

financing of the buyouts.

One of the final major buyouts of the 1980s proved to be its most ambitious and marked both a high water mark and a sign of the beginning of the end of the boom that had begun nearly a decade earlier. In 1989, KKR closed in on a $31.1 billion dollar takeover of RJR Nabisco

. It was, at that time and for over 17 years, the largest leverage buyout in history. The event was chronicled in the book (and later the movie), Barbarians at the Gate: The Fall of RJR Nabisco

. KKR would eventually prevail in acquiring RJR Nabisco at $109 per share marking a dramatic increase from the original announcement that Shearson Lehman Hutton would take RJR Nabisco private at $75 per share. A fierce series of negotiations and horse-trading ensued which pitted KKR against Shearson Lehman Hutton and later Forstmann Little & Co. Many of the major banking players of the day, including Morgan Stanley

, Goldman Sachs

, Salomon Brothers

, and Merrill Lynch

were actively involved in advising and financing the parties. After Shearson Lehman's original bid, KKR quickly introduced a tender offer to obtain RJR Nabisco for $90 per share—a price that enabled it to proceed without the approval of RJR Nabisco's management. RJR's management team, working with Shearson Lehman and Salomon Brothers

, submitted a bid of $112, a figure they felt certain would enable them to outflank any response by Kravis's team. KKR's final bid of $109, while a lower dollar figure, was ultimately accepted by the board of directors of RJR Nabisco. At $31.1 billion of transaction value, RJR Nabisco was by far the largest leveraged buyout in history. In 2006 and 2007, a number of leveraged buyout transactions were completed that for the first time surpassed the RJR Nabisco leveraged buyout in terms of nominal purchase price. However, adjusted for inflation, none of the leveraged buyouts of the 2006–2007 period would surpass RJR Nabisco.

By the end of the 1980s the excesses of the buyout market were beginning to show, with the bankruptcy

of several large buyouts including Robert Campeau

's 1988 buyout of Federated Department Stores

, the 1986 buyout of the Revco

drug stores, Walter Industries, FEB Trucking and Eaton Leonard. Additionally, the RJR Nabisco deal was showing signs of strain, leading to a recapitalization in 1990 that involved the contribution of $1.7 billion of new equity from KKR.

Drexel Burnham Lambert

was the investment bank most responsible for the boom in private equity during the 1980s due to its leadership in the issuance of high-yield debt

.

Drexel reached an agreement with the government in which it pleaded nolo contendere

(no contest) to six felonies—three counts of stock parking and three counts of stock manipulation. It also agreed to pay a fine of $650 million—at the time, the largest fine ever levied under securities laws. Milken left the firm after his own indictment in March 1989. On February 13, 1990 after being advised by United States Secretary of the Treasury

Nicholas F. Brady

, the U.S. Securities and Exchange Commission (SEC), the New York Stock Exchange

, and the Federal Reserve, Drexel Burnham Lambert

officially filed for Chapter 11 bankruptcy protection.

) would set the stage for the largest boom private equity had seen. Marked by the buyout of Dex Media

in 2002, large multi-billion dollar U.S. buyouts could once again obtain significant high yield debt financing and larger transactions could be completed. By 2004 and 2005, major buyouts were once again becoming common, including the acquisitions of Toys "R" Us, The Hertz Corporation

, Metro-Goldwyn-Mayer

and SunGard

in 2005.

As 2005 ended and 2006 began, new "largest buyout" records were set and surpassed several times with nine of the top ten buyouts at the end of 2007 having been announced in an 18-month window from the beginning of 2006 through the middle of 2007. In 2006, private equity firms bought 654 U.S. companies for $375 billion, representing 18 times the level of transactions closed in 2003. Additionally, U.S. based private equity firms raised $215.4 billion in investor commitments to 322 funds, surpassing the previous record set in 2000 by 22% and 33% higher than the 2005 fundraising total The following year, despite the onset of turmoil in the credit markets in the summer, saw yet another record year of fundraising with $302 billion of investor commitments to 415 funds Among the mega-buyouts completed during the 2006 to 2007 boom were: Equity Office Properties, HCA

, Alliance Boots

and TXU

.

In July 2007, turmoil that had been affecting the mortgage markets

spilled over into the leveraged finance

and high-yield debt

markets. The markets had been highly robust during the first six months of 2007, with highly issuer friendly developments including PIK and PIK Toggle

(interest is "Payable In Kind") and covenant light

debt widely available to finance large leveraged buyouts. July and August saw a notable slowdown in issuance levels in the high yield and leveraged loan markets with only few issuers accessing the market. Uncertain market conditions led to a significant widening of yield spreads, which coupled with the typical summer slowdown led to many companies and investment banks to put their plans to issue debt on hold until the autumn. However, the expected rebound in the market after Labor Day

2007 did not materialize and the lack of market confidence prevented deals from pricing. By the end of September, the full extent of the credit situation became obvious as major lenders including Citigroup

and UBS AG

announced major writedowns due to credit losses. The leveraged finance markets came to a near standstill. As 2007 ended and 2008 began, it was clear that lending standards had tightened and the era of "mega-buyouts" had come to an end. Nevertheless, private equity continues to be a large and active asset class and the private equity firms, with hundreds of billions of dollars of committed capital from investors are looking to deploy capital in new and different transactions.

Germany

currently introduces new tax laws, taxing parts of the cash flow before debt interest deduction. The motivation for the change is to discourage leveraged buyouts by reducing the tax shield effectiveness.

Historically, many LBOs in the 1980s and 1990s focused on reducing wasteful expenditures by corporate managers whose interests were not aligned with shareholders. After a major corporate restructuring, which may involve selling off portions of the company and severe staff reductions, the entity would likely be producing a higher income stream. Because this type of management arbitrage

and easy restructuring has largely been accomplished, LBOs today focus more on growth and complicated financial engineering to achieve their returns. Most leveraged buyout firms look to achieve an internal rate of return

in excess of 20%.

(MBO), which occurs when a company's managers buy or acquire a large part of the company. The goal of an MBO may be to strengthen the managers' interest in the success of the company. In most cases when the company is initially listed, the management will then make it private. MBOs have assumed an important role in corporate restructurings beside mergers and acquisitions

. Key considerations in an MBO are fairness to shareholders, price, the future business plan

, and legal and tax issues. One recent criticism of MBOs is that they create a conflict of interest—an incentive is created for managers to mismanage (or not manage as efficiently) a company, thereby depressing its stock price, and profiting handsomely by implementing effective management after the successful MBO, as Paul Newman's character attempted in the Coen brothers' film The Hudsucker Proxy

.

Of course, the incentive to artificially reduce share price extends beyond management buyouts.

It may be fairly easy for a top executive to reduce the price of his/her company's stock - due

to information asymmetry

. The executive can accelerate accounting of expected expenses, delay accounting of expected revenue, engage in off balance sheet transactions to make the company's profitability appear temporarily poorer, or simply promote and report severely conservative (e.g. pessimistic) estimates of future earnings. Such seemingly adverse earnings

news will be likely to (at least temporarily) reduce share price. (This is again due to information asymmetries since it is more common for top executives to do everything they can to window dress

their company's earnings forecasts).

A reduced share price makes a company an easier takeover

target. When the company gets bought out (or taken private) - at a dramatically lower price - the takeover

artist gains a windfall from the former top executive's actions to surreptitiously reduce share price. This can represent tens of billions of dollars (questionably) transferred from previous shareholders to the takeover artist. The former top executive is then rewarded with a golden parachute

for presiding over the firesale that can sometimes be in the hundreds of millions of dollars for one or two years of work.

(This is nevertheless an excellent bargain for the takeover artist, who will tend to benefit from developing a reputation of being very generous to parting top executives).

Similar issues occur when a publicly held asset or non-profit organization undergoes privatization

.

Top executives often reap tremendous monetary benefits when a government owned or non-profit entity

is sold to private hands. Just as in the example above, they can facilitate this process by making the

entity appear to be in financial crisis - this reduces the sale price (to the profit of the purchaser), and makes non-profits and governments more likely to sell. Ironically, it can also contribute to a public perception that private entities are more efficiently run reinforcing the political will to sell of public assets.

Again, due to asymmetric information, policy makers and the general public see a government owned firm

that was a financial 'disaster' - miraculously turned around by the private sector (and typically resold) within a few years.

Nevertheless, the incentive to artificially reduce the share price of a firm is higher

for management buyouts, than for other forms of takeovers or LBOs.

, such as Robert Campeau

's 1988 buyout of Federated Department Stores

and the 1986 buyout of the Revco

drug stores. The failure of the Federated buyout was a result of excessive debt financing, comprising about 97% of the total consideration, which led to large interest payments that exceeded the company's operating cash flow. In response to the threat of LBOs, certain companies adopted a number of techniques, such as the poison pill

, to protect them against hostile takeovers by effectively self-destructing the company if it were to be taken over.

The inability to repay debt in an LBO can be caused by initial overpricing of the target firm and/or its assets. Because LBO funds often attempt to increase the value of an acquired company by liquidating certain assets or selling underperforming business units

, the bought-out firm may face insolvency

as depleted operating revenues become insufficient to repay the debt. Over-optimistic forecasts of the revenues of the target company may also lead to financial distress

after acquisition. Some courts have found that LBO debt constitutes a fraudulent transfer

under U.S. insolvency law if it is determined to be the cause of the acquired firm's failure.

However, the Bankruptcy Code

includes a so-called "safe harbor" provision, preventing bankruptcy trustees from recovering settlement payments to the bought-out shareholders. In 2009, the U.S. Court of Appeals for the Sixth Circuit held that such settlement payments could not be avoided, irrespective of whether they occurred in an LBO of a public or private company.

s (i.e. a leveraged buyout of a company that was acquired through a leveraged buyout). A secondary buyout will often provide a clean break for the selling private equity firms and its limited partner investors. Historically, however, secondary buyouts were perceived as distressed sales by both seller and buyer, were considered unattractive by limited partner investors and were largely avoided.

The increase in secondary buyout activity in 2000s was driven in large part by an increase in capital in the leveraged buyout space. Often, selling private equity firms will pursue a secondary buyout for a number of reasons:

Often, secondary buyouts have been successful if the investment has reached an age where it is necessary or desirable to sell rather than hold the investment further or where the investment had already generated significant value for the selling firm.

Secondary buyouts differ from secondaries

or secondary market purchases

which typically involve the acquisition of portfolios of private equity assets including limited partnership stakes and direct investments in corporate securities.

, based on the company's forecasted financial performance. LBO analysis typically builds upon a medium-term forecast (typical investment horizon for financial sponsors is 3–7 years) to project future operating results.

The analysis works similarly, in many respects, to a discounted cash flow

. The analysis will project the debt repaid by the company during the forecast period and make assumptions about the multiple of earnings at which the business will be sold after a period of time. By targeting returns consistent with historical targets for private equity firms, the LBO analysis will provide an estimate of what purchase price a buyer would be willing to pay to achieve those returns.

and the film adaptation

, based on actual events, a fictional LBO is the basis of the 1963 Japanese film High and Low.

Financial sponsor

A financial sponsor is a term commonly used to refer to private equity investment firms, particularly those private equity firms that engage in leveraged buyout or LBO transactions....

, acquires a controlling interest

Controlling interest

Controlling interest in a corporation means to have control of a large enough block of voting stock shares in a company such that no one stock holder or coalition of stock holders can successfully oppose a motion...

in a company's equity

Ownership equity

In accounting and finance, equity is the residual claim or interest of the most junior class of investors in assets, after all liabilities are paid. If liability exceeds assets, negative equity exists...

and where a significant percentage of the purchase price is financed through leverage

Leverage (finance)

In finance, leverage is a general term for any technique to multiply gains and losses. Common ways to attain leverage are borrowing money, buying fixed assets and using derivatives. Important examples are:* A public corporation may leverage its equity by borrowing money...

(borrowing

Debt

A debt is an obligation owed by one party to a second party, the creditor; usually this refers to assets granted by the creditor to the debtor, but the term can also be used metaphorically to cover moral obligations and other interactions not based on economic value.A debt is created when a...

). The assets of the acquired company are used as collateral for the borrowed capital, sometimes with assets of the acquiring company. Typically, leveraged buyout uses a combination of various debt instruments from bank and debt capital markets. The bonds or other paper issued for leveraged buyouts are commonly considered not to be investment grade because of the significant risks involved. If the company subsequently defaults on its debts, the LBO transaction will frequently be challenged by creditors or a bankruptcy trustee under a theory of fraudulent transfer

Fraudulent conveyance

A fraudulent conveyance, or fraudulent transfer, is a civil cause of action. It arises in debtor/creditor relations, particularly with reference to insolvent debtors. The cause of action is typically brought by creditors or by bankruptcy trustees...

Companies of all sizes and industries have been the target of leveraged buyout transactions, although because of the importance of debt and the ability of the acquired firm to make regular loan payments after the completion of a leveraged buyout, some features of potential target firms make for more attractive leverage buyout candidates, including:

- Low existing debt loads;

- A multi-year history of stable and recurring cash flows;

- Hard assets (property, plant and equipment, inventoryInventoryInventory means a list compiled for some formal purpose, such as the details of an estate going to probate, or the contents of a house let furnished. This remains the prime meaning in British English...

, receivablesAccounts receivableAccounts receivable also known as Debtors, is money owed to a business by its clients and shown on its Balance Sheet as an asset...

) that may be used as collateral for lower cost secured debt; - The potential for new management to make operational or other improvements to the firm to boost cash flows, such as workforce reductions or eliminations;

- Market conditions and perceptions that depress the valuation or stock price.

Characteristics

Financial sponsor

A financial sponsor is a term commonly used to refer to private equity investment firms, particularly those private equity firms that engage in leveraged buyout or LBO transactions....

s (like a private equity firm

Private equity firm

A private equity firm is an investment manager that makes investments in the private equity of operating companies through a variety of loosely affiliated investment strategies including leveraged buyout, venture capital, and growth capital...

) making large acquisitions without committing all the capital required for the acquisition. To do this, a financial sponsor will raise acquisition debt (by issuing bonds or securing a loan) which is ultimately secured upon the acquisition target and also looks to the cash flows of the acquisition target to make interest and principal payments. Acquisition debt in an LBO is therefore usually non-recourse

Nonrecourse debt

Non-recourse debt or a non-recourse loan is a secured loan that is secured by a pledge of collateral, typically real property, but for which the borrower is not personally liable. If the borrower defaults, the lender/issuer can seize the collateral, but the lender's recovery is limited to the...

to the financial sponsor and to the equity fund that the financial sponsor manages. Furthermore, unlike in a hedge fund, where debt raised to purchase certain securities is also collateralized by the fund's other securities, the acquisition debt in an LBO is recourse only to the company purchased in a particular LBO transaction. Therefore, an LBO transaction's financial structure is particularly attractive to a fund's limited partners, allowing them the benefits of leverage but greatly limiting the degree of recourse of that leverage.

This kind of acquisition brings leverage benefits to an LBO's financial sponsor in two ways: (1) the investor itself only needs to provide a fraction of the capital for the acquisition, and (2) assuming the economic internal rate of return on the investment (taking into account expected exit proceeds) exceeds the weighted average interest rate on the acquisition debt, returns to the financial sponsor will be significantly enhanced.

As transaction sizes grow, the equity component of the purchase price can be provided by multiple financial sponsors "co-investing" to come up with the needed equity for a purchase. Likewise, multiple lenders may band together in a "syndicate" to jointly provide the debt required to fund the transaction. Today, larger transactions are dominated by dedicated private equity

Private equity

Private equity, in finance, is an asset class consisting of equity securities in operating companies that are not publicly traded on a stock exchange....

firms and a limited number of large banks with "financial sponsors" groups.

As a percentage of the purchase price for a leverage buyout target, the amount of debt used to finance a transaction varies according to the financial condition and history of the acquisition target, market conditions, the willingness of lenders

Bank

A bank is a financial institution that serves as a financial intermediary. The term "bank" may refer to one of several related types of entities:...

to extend credit (both to the LBO's financial sponsor

Financial sponsor

A financial sponsor is a term commonly used to refer to private equity investment firms, particularly those private equity firms that engage in leveraged buyout or LBO transactions....

s and the company to be acquired) as well as the interest costs and the ability of the company to cover those costs. Typically the debt portion of a LBO ranges from 50%-85% of the purchase price, but in some cases debt may represent upwards of 95% of purchase price. Between 2000-2005 debt averaged between 59.4% and 67.9% of total purchase price for LBOs in the United States.

To finance LBO's, private-equity firms usually issue some combination of syndicated loan

Syndicated loan

A syndicated loan is one that is provided by a group of lenders and is structured, arranged, and administered by one or several commercial banks or investment banks known as arrangers....

s and high-yield bonds. Smaller transactions may also be financed with mezzanine debt from insurance companies or specialty lenders. Syndicated loans are typically arranged by investment banks and financed by commercial banks and loan fund managers, such as mutual funds, hedge funds, credit opportunity investors and structured finance vehicles. The commercial banks typically provide revolving credit

Revolving credit

Revolving credit is a type of credit that does not have a fixed number of payments, in contrast to installment credit. Examples of revolving credits used by consumers include credit cards. Corporate revolving credit facilities are typically used to provide liquidity for a company's day-to-day...

s that provide issuers with liquidity and cash flow while fund managers generally provided funded term loans that are used to finance the LBO. These loans tend to be senior secured, floating-rate instruments pegged to the London Interbank Offered Rate

London Interbank Offered Rate

The LIBOR rate is the average interest rate that leading banks in London charge when lending to other banks. It is an acronym for London Interbank Offered Rate Banks borrow money for one day, one month, two months, six months, one year etc. and they pay interest to their lenders based on...

(LIBOR). They are typically pre-payable at the option of the issuer, though in some cases modest prepayment fees apply. High-yield bonds, meanwhile, are also underwritten by investment banks but are financed by a combination of retail and institutional credit investors, including high-yield mutual funds, hedge funds, credit opportunities and other institutional accounts. High-yield bonds tend to be fixed-rate instruments. Most are unsecured, though in some cases issuers will sell senior secured notes. The bonds usually have no-call periods of 3–5 years and then high prepayment fees thereafter. Issuers, however, will in many cases have a "claw-back option" that allows them to repay some percentage during the no-call period (usually 35%) with equity proceeds.

Another source of financing for LBO's is seller's notes, which are provided in some cases by the entity as a way to facilitate the transaction.

History

Origins of the leveraged buyouts

The first leveraged buyout may have been the purchase by McLean Industries, Inc. of Pan-Atlantic Steamship Company in January 1955 and Waterman Steamship CorporationWaterman Steamship Corporation

Waterman Steamship Corporation is an American deep sea ocean carrier, specializing in liner services and time charter contracts. It is owned by International Shipholding Corporation, based in Mobile, Alabama....

in May 1955. Under the terms of that transaction, McLean borrowed $42 million and raised an additional $7 million through an issue of preferred stock

Preferred stock

Preferred stock, also called preferred shares, preference shares, or simply preferreds, is a special equity security that has properties of both an equity and a debt instrument and is generally considered a hybrid instrument...

. When the deal closed, $20 million of Waterman cash and assets were used to retire $20 million of the loan debt.

Similar to the approach employed in the McLean transaction, the use of publicly traded holding companies as investment vehicles to acquire portfolios of investments in corporate assets was a relatively new trend in the 1960s, popularized by the likes of Warren Buffett

Warren Buffett

Warren Edward Buffett is an American business magnate, investor, and philanthropist. He is widely regarded as one of the most successful investors in the world. Often introduced as "legendary investor, Warren Buffett", he is the primary shareholder, chairman and CEO of Berkshire Hathaway. He is...

(Berkshire Hathaway

Berkshire Hathaway

Berkshire Hathaway Inc. is an American multinational conglomerate holding company headquartered in Omaha, Nebraska, United States, that oversees and manages a number of subsidiary companies. The company averaged an annual growth in book value of 20.3% to its shareholders for the last 44 years,...

) and Victor Posner

Victor Posner

Victor Posner was an American businessman. He was known as one of the highest paid business executives of his generation. He was a pioneer of the leveraged buyout.-Career:...

(DWG Corporation), and later adopted by Nelson Peltz

Nelson Peltz

Nelson Peltz is an American businessman. He is a board director of Wendy's Group, the franchise parent of T.J. Cinnamons, Pasta Connection and Wendy's. Peltz is the former owner of Snapple.- Background :...

(Triarc), Saul Steinberg

Saul Steinberg (business)

Saul Steinberg is a former financier, insurance executive, and corporate raider. He started a computer leasing company , which he used in an audacious and successful takeover of the much larger Reliance Insurance Company in 1968...

(Reliance Insurance) and Gerry Schwartz

Gerry Schwartz

Gerald W. Schwartz, OC born c.1941 in Winnipeg, Manitoba, is a Canadian businessman. In 1977 he co-founded CanWest Global Communications Inc, followed by Onex Corporation in 1983. He has been a director of Scotiabank since 1999...

(Onex Corporation). These investment vehicles would utilize a number of the same tactics and target the same type of companies as more traditional leveraged buyouts and in many ways could be considered a forerunner of the later private equity firms. In fact it is Posner who is often credited with coining the term "leveraged buyout" or "LBO"

The leveraged buyout boom of the 1980s was conceived by a number of corporate financiers, most notably Jerome Kohlberg, Jr.

Jerome Kohlberg, Jr.

Jerome Kohlberg, Jr. is an American businessman and early pioneer in the private equity and leveraged buyout industries founding private equity firm Kohlberg Kravis Roberts & Co. and later Kohlberg & Company....

and later his protégé Henry Kravis

Henry Kravis

Henry R. Kravis is an American businessman and private equity investor. He is the co-founder of Kohlberg Kravis Roberts & Co., a private equity firm with over $62 billion in assets as of 2011. He has an estimated net worth of $3.7 billion as of September 2011, ranked by Forbes as the 88th richest...

. Working for Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

at the time, Kohlberg and Kravis, along with Kravis' cousin George Roberts

George R. Roberts

George R. Roberts is an American financier and was one of the three original partners of Kohlberg Kravis Roberts & Co. , which he co-founded alongside Jerome Kohlberg and first cousin Henry Kravis in 1976.-Biography:...

, began a series of what they described as "bootstrap" investments. Many of the target companies lacked a viable or attractive exit for their founders, as they were too small to be taken public and the founders were reluctant to sell out to competitors. Thus a sale to a financial buyer

Financial sponsor

A financial sponsor is a term commonly used to refer to private equity investment firms, particularly those private equity firms that engage in leveraged buyout or LBO transactions....

might prove attractive. Their acquisition of Orkin Exterminating Company

Orkin

Orkin is a pest-control company that is a wholly owned subsidiary of Rollins Inc.-The Orkin Uniform:The most recognized Orkin uniform consists of a white collared shirt with the Orkin logo and red epaulets and pressed khaki pants. The uniform varies depending on an employee’s job function for...

in 1964 is among the first significant leveraged buyout transactions.. In the following years the three Bear Stearns

Bear Stearns

The Bear Stearns Companies, Inc. based in New York City, was a global investment bank and securities trading and brokerage, until its sale to JPMorgan Chase in 2008 during the global financial crisis and recession...

bankers would complete a series of buyouts including Stern Metals (1965), Incom (a division of Rockwood International, 1971), Cobblers Industries (1971), and Boren Clay (1973) as well as Thompson Wire, Eagle Motors and Barrows through their investment in Stern Metals. By 1976, tensions had built up between Bear Stearns and Kohlberg, Kravis and Roberts leading to their departure and the formation of Kohlberg Kravis Roberts in that year.

Leveraged buyouts in the 1980s

In January 1982, former US Secretary of the Treasury William Simon and a group of investors acquired Gibson Greetings, a producer of greeting cards, for $80 million, of which only $1 million was rumored to have been contributed by the investors. By mid-1983, just sixteen months after the original deal, Gibson completed a $290 million IPO and Simon made approximately $66 million. The success of the Gibson Greetings investment attracted the attention of the wider media to the nascent boom in leveraged buyouts. Between 1979 and 1989, it was estimated that there were over 2,000 leveraged buyouts valued in excess of $250 billionDuring the 1980s, constituencies within acquired companies and the media ascribed the "corporate raid

Corporate raid

A corporate raid is an American English business term for buying a large interest in a corporation and then using voting rights to enact measures directed at increasing the share value...

" label to many private equity investments, particularly those that featured a hostile takeover of the company, perceived asset stripping

Asset stripping

Asset stripping involves selling the assets of a business individually at a profit. The term is generally used in a pejorative sense as such activity is not considered productive to the economy. Asset stripping is considered to be a problem in economies such as Russia or China that are making a...

, major layoffs or other significant corporate restructuring activities. Among the most notable investors to be labeled corporate raiders in the 1980s included Carl Icahn

Carl Icahn

Carl Celian Icahn is an American business magnate and investor.-Biography:Icahn was raised in Far Rockaway, Queens, New York City, where he attended Far Rockaway High School. His father was a cantor, his mother was a schoolteacher...

, Victor Posner

Victor Posner

Victor Posner was an American businessman. He was known as one of the highest paid business executives of his generation. He was a pioneer of the leveraged buyout.-Career:...

, Nelson Peltz

Nelson Peltz

Nelson Peltz is an American businessman. He is a board director of Wendy's Group, the franchise parent of T.J. Cinnamons, Pasta Connection and Wendy's. Peltz is the former owner of Snapple.- Background :...

, Robert M. Bass

Robert Bass

Robert Muse Bass is an American businessman and philanthropist. He is currently the chairman of Aerion Corporation, an American aerospace firm in Reno, Nevada. Bass is worth approximately $5.5 billion as of 2007, and $4 billion in 2010 on oil and other investments-Life:Bass was born into a wealthy...

, T. Boone Pickens, Harold Clark Simmons

Harold Clark Simmons

Harold Clark Simmons is an American businessman and billionaire whose banking expertise helped him develop the acquisition concept known as the leveraged buyout to acquire various corporations. He is the owner of Contran Corporation and of Valhi, Inc.,...

, Kirk Kerkorian

Kirk Kerkorian

Kerkor "Kirk" Kerkorian is an American businessman who is the president/CEO of Tracinda Corporation, his private holding company based in Beverly Hills, California. Kerkorian is known as one of the important figures in shaping Las Vegas and, with architect Martin Stern, Jr...

, Sir James Goldsmith, Saul Steinberg

Saul Steinberg (business)

Saul Steinberg is a former financier, insurance executive, and corporate raider. He started a computer leasing company , which he used in an audacious and successful takeover of the much larger Reliance Insurance Company in 1968...

and Asher Edelman

Asher Edelman

Asher Edelman began his career on Wall Street in 1961. In 1969 he formed Mack, Bushnell and Edelman where he was CEO. Edelman’s Wall Street businesses included Investment Banking, Money Management, and Derivatives Trading...

. Carl Icahn

Carl Icahn

Carl Celian Icahn is an American business magnate and investor.-Biography:Icahn was raised in Far Rockaway, Queens, New York City, where he attended Far Rockaway High School. His father was a cantor, his mother was a schoolteacher...

developed a reputation as a ruthless corporate raider after his hostile takeover of TWA

Trans World Airlines

Trans World Airlines was an American airline that existed from 1925 until it was bought out by and merged with American Airlines in 2001. It was a major domestic airline in the United States and the main U.S.-based competitor of Pan American World Airways on intercontinental routes from 1946...

in 1985. Many of the corporate raiders were onetime clients of Michael Milken

Michael Milken

Michael Robert Milken is an American business magnate, financier, and philanthropist noted for his role in the development of the market for high-yield bonds during the 1970s and 1980s, for his 1990 guilty plea to felony charges for violating US securities laws, and for his funding of medical...

, whose investment banking firm, Drexel Burnham Lambert

Drexel Burnham Lambert

Drexel Burnham Lambert was a major Wall Street investment banking firm, which first rose to prominence and then was forced into bankruptcy in February 1990 by its involvement in illegal activities in the junk bond market, driven by Drexel employee Michael Milken. At its height, it was the...

helped raise blind pools of capital with which corporate raiders could make a legitimate attempt to take over a company and provided high-yield debt

High-yield debt

In finance, a high-yield bond is a bond that is rated below investment grade...

financing of the buyouts.

One of the final major buyouts of the 1980s proved to be its most ambitious and marked both a high water mark and a sign of the beginning of the end of the boom that had begun nearly a decade earlier. In 1989, KKR closed in on a $31.1 billion dollar takeover of RJR Nabisco

RJR Nabisco

RJR Nabisco, Inc., was an American conglomerate formed in 1985 by the merger of Nabisco Brands and R.J. Reynolds Tobacco Company. RJR Nabisco was purchased in 1988 by Kohlberg Kravis Roberts & Co...

. It was, at that time and for over 17 years, the largest leverage buyout in history. The event was chronicled in the book (and later the movie), Barbarians at the Gate: The Fall of RJR Nabisco

Barbarians at the Gate: The Fall of RJR Nabisco

Barbarians at the Gate: The Fall of RJR Nabisco is a 1990 book about the leveraged buyout of RJR Nabisco, written by investigative journalists Bryan Burrough and John Helyar. The book is based upon a series of articles written by the authors for The Wall Street Journal...

. KKR would eventually prevail in acquiring RJR Nabisco at $109 per share marking a dramatic increase from the original announcement that Shearson Lehman Hutton would take RJR Nabisco private at $75 per share. A fierce series of negotiations and horse-trading ensued which pitted KKR against Shearson Lehman Hutton and later Forstmann Little & Co. Many of the major banking players of the day, including Morgan Stanley

Morgan Stanley

Morgan Stanley is a global financial services firm headquartered in New York City serving a diversified group of corporations, governments, financial institutions, and individuals. Morgan Stanley also operates in 36 countries around the world, with over 600 offices and a workforce of over 60,000....

, Goldman Sachs

Goldman Sachs

The Goldman Sachs Group, Inc. is an American multinational bulge bracket investment banking and securities firm that engages in global investment banking, securities, investment management, and other financial services primarily with institutional clients...

, Salomon Brothers

Salomon Brothers

Salomon Brothers was a bulge bracket, Wall Street investment bank. Founded in 1910 by three brothers along with a clerk named Ben Levy, it remained a partnership until the early 1980s, when it was acquired by the commodity trading firm Phibro Corporation and then became Salomon Inc. Eventually...

, and Merrill Lynch

Merrill Lynch

Merrill Lynch is the wealth management division of Bank of America. With over 15,000 financial advisors and $2.2 trillion in client assets it is the world's largest brokerage. Formerly known as Merrill Lynch & Co., Inc., prior to 2009 the firm was publicly owned and traded on the New York...

were actively involved in advising and financing the parties. After Shearson Lehman's original bid, KKR quickly introduced a tender offer to obtain RJR Nabisco for $90 per share—a price that enabled it to proceed without the approval of RJR Nabisco's management. RJR's management team, working with Shearson Lehman and Salomon Brothers

Salomon Brothers

Salomon Brothers was a bulge bracket, Wall Street investment bank. Founded in 1910 by three brothers along with a clerk named Ben Levy, it remained a partnership until the early 1980s, when it was acquired by the commodity trading firm Phibro Corporation and then became Salomon Inc. Eventually...

, submitted a bid of $112, a figure they felt certain would enable them to outflank any response by Kravis's team. KKR's final bid of $109, while a lower dollar figure, was ultimately accepted by the board of directors of RJR Nabisco. At $31.1 billion of transaction value, RJR Nabisco was by far the largest leveraged buyout in history. In 2006 and 2007, a number of leveraged buyout transactions were completed that for the first time surpassed the RJR Nabisco leveraged buyout in terms of nominal purchase price. However, adjusted for inflation, none of the leveraged buyouts of the 2006–2007 period would surpass RJR Nabisco.

By the end of the 1980s the excesses of the buyout market were beginning to show, with the bankruptcy

Bankruptcy

Bankruptcy is a legal status of an insolvent person or an organisation, that is, one that cannot repay the debts owed to creditors. In most jurisdictions bankruptcy is imposed by a court order, often initiated by the debtor....

of several large buyouts including Robert Campeau

Robert Campeau

Robert Campeau is a Canadian financier and real estate developer.-Early years:His formal education ended in grade eight, at the age of 14. He talked himself into jobs at Inco as a general labourer, carpenter and machinist. In 1949 he entered the residential end of the construction business...

's 1988 buyout of Federated Department Stores

Federated Department Stores

Macy's, Inc. is a department store holding company and owner of Macy's and Bloomingdale's department stores. Macy's Inc.'s stores specialize mostly in retail clothing, jewelery, watches, dinnerware, and furniture....

, the 1986 buyout of the Revco

Revco

Revco Discount Drug Stores , once based in Twinsburg, Ohio, was a major drug store chain operating through the Ohio Valley, the Mid-Atlantic states, and the Southeastern United States. The chain's stock was traded on the New York Stock Exchange under the ticker RXR...

drug stores, Walter Industries, FEB Trucking and Eaton Leonard. Additionally, the RJR Nabisco deal was showing signs of strain, leading to a recapitalization in 1990 that involved the contribution of $1.7 billion of new equity from KKR.

Drexel Burnham Lambert

Drexel Burnham Lambert

Drexel Burnham Lambert was a major Wall Street investment banking firm, which first rose to prominence and then was forced into bankruptcy in February 1990 by its involvement in illegal activities in the junk bond market, driven by Drexel employee Michael Milken. At its height, it was the...

was the investment bank most responsible for the boom in private equity during the 1980s due to its leadership in the issuance of high-yield debt

High-yield debt

In finance, a high-yield bond is a bond that is rated below investment grade...

.

Drexel reached an agreement with the government in which it pleaded nolo contendere

Nolo contendere

is a legal term that comes from the Latin for "I do not wish to contend." It is also referred to as a plea of no contest.In criminal trials, and in some common law jurisdictions, it is a plea where the defendant neither admits nor disputes a charge, serving as an alternative to a pleading of...

(no contest) to six felonies—three counts of stock parking and three counts of stock manipulation. It also agreed to pay a fine of $650 million—at the time, the largest fine ever levied under securities laws. Milken left the firm after his own indictment in March 1989. On February 13, 1990 after being advised by United States Secretary of the Treasury

United States Secretary of the Treasury

The Secretary of the Treasury of the United States is the head of the United States Department of the Treasury, which is concerned with financial and monetary matters, and, until 2003, also with some issues of national security and defense. This position in the Federal Government of the United...

Nicholas F. Brady

Nicholas F. Brady

Nicholas Frederick Brady was United States Secretary of the Treasury under Presidents Ronald Reagan and George H. W. Bush, and is also known for articulating the Brady Plan in March 1989.-Early life:...

, the U.S. Securities and Exchange Commission (SEC), the New York Stock Exchange

New York Stock Exchange

The New York Stock Exchange is a stock exchange located at 11 Wall Street in Lower Manhattan, New York City, USA. It is by far the world's largest stock exchange by market capitalization of its listed companies at 13.39 trillion as of Dec 2010...

, and the Federal Reserve, Drexel Burnham Lambert

Drexel Burnham Lambert

Drexel Burnham Lambert was a major Wall Street investment banking firm, which first rose to prominence and then was forced into bankruptcy in February 1990 by its involvement in illegal activities in the junk bond market, driven by Drexel employee Michael Milken. At its height, it was the...

officially filed for Chapter 11 bankruptcy protection.

Age of the mega-buyout 2005-2007

The combination of decreasing interest rates, loosening lending standards and regulatory changes for publicly traded companies (specifically the Sarbanes-Oxley ActSarbanes-Oxley Act

The Sarbanes–Oxley Act of 2002 , also known as the 'Public Company Accounting Reform and Investor Protection Act' and 'Corporate and Auditing Accountability and Responsibility Act' and commonly called Sarbanes–Oxley, Sarbox or SOX, is a United States federal law enacted on July 30, 2002, which...

) would set the stage for the largest boom private equity had seen. Marked by the buyout of Dex Media

Dex Media

Dex Media, Inc. was a print and interactive marketing company. It was acquired by R.H. Donnelley, which became Dex One Corporation in February 2010...

in 2002, large multi-billion dollar U.S. buyouts could once again obtain significant high yield debt financing and larger transactions could be completed. By 2004 and 2005, major buyouts were once again becoming common, including the acquisitions of Toys "R" Us, The Hertz Corporation

The Hertz Corporation

Hertz Global Holdings Inc is an American car rental company with international locations in 145 countries worldwide.-Early years:The company was founded by Walter L. Jacobs in 1918, who started a car rental operation in Chicago with a dozen Model T Ford cars. In 1923, Jacobs sold it to John D...

, Metro-Goldwyn-Mayer

Metro-Goldwyn-Mayer

Metro-Goldwyn-Mayer Inc. is an American media company, involved primarily in the production and distribution of films and television programs. MGM was founded in 1924 when the entertainment entrepreneur Marcus Loew gained control of Metro Pictures, Goldwyn Pictures Corporation and Louis B. Mayer...

and SunGard

SunGard

SunGard is a multinational company based in Wayne, Pennsylvania, which provides software and services to education, financial services, and public sector organizations. It was formed in 1983, as a spin-off of the computer services division of Sun Oil Company, during a period of low crude oil...

in 2005.

As 2005 ended and 2006 began, new "largest buyout" records were set and surpassed several times with nine of the top ten buyouts at the end of 2007 having been announced in an 18-month window from the beginning of 2006 through the middle of 2007. In 2006, private equity firms bought 654 U.S. companies for $375 billion, representing 18 times the level of transactions closed in 2003. Additionally, U.S. based private equity firms raised $215.4 billion in investor commitments to 322 funds, surpassing the previous record set in 2000 by 22% and 33% higher than the 2005 fundraising total The following year, despite the onset of turmoil in the credit markets in the summer, saw yet another record year of fundraising with $302 billion of investor commitments to 415 funds Among the mega-buyouts completed during the 2006 to 2007 boom were: Equity Office Properties, HCA

Hospital Corporation of America

Hospital Corporation of America is the largest private operator of health care facilities in the world, It is based in Nashville, Tennessee and is widely considered to be the single largest factor in making that city a hotspot for healthcare enterprise.-History:The founders of HCA include Jack C....

, Alliance Boots

Alliance Boots

Alliance Boots GmbH is a leading international, pharmacy-led health and beauty group. It has two core business activities - pharmacy-led health and beauty retailing, and pharmaceutical wholesaling and distribution - and has a presence in more than 25 countries...

and TXU

TXU

Energy Future Holdings Corporation is an electric utility company headquartered in Energy Plaza in Downtown Dallas, Texas, United States. The company was known as TXU until its $45 billion leveraged buyout by Kohlberg Kravis Roberts, Texas Pacific Group and Goldman Sachs...

.

In July 2007, turmoil that had been affecting the mortgage markets

Subprime mortgage crisis

The U.S. subprime mortgage crisis was one of the first indicators of the late-2000s financial crisis, characterized by a rise in subprime mortgage delinquencies and foreclosures, and the resulting decline of securities backed by said mortgages....

spilled over into the leveraged finance

Leverage (finance)

In finance, leverage is a general term for any technique to multiply gains and losses. Common ways to attain leverage are borrowing money, buying fixed assets and using derivatives. Important examples are:* A public corporation may leverage its equity by borrowing money...

and high-yield debt

High-yield debt

In finance, a high-yield bond is a bond that is rated below investment grade...

markets. The markets had been highly robust during the first six months of 2007, with highly issuer friendly developments including PIK and PIK Toggle

PIK loan

A PIK loan is a type of loan which typically does not provide for any cash flows from borrower to lender between the drawdown date and the maturity or refinancing date, not even interest or parts thereof , thus making it an expensive, high-risk financing instrument...

(interest is "Payable In Kind") and covenant light

Cov-lite

Cov-lite is financial jargon for loan agreements which do not contain the usual protective covenants for the benefit of the lending party...

debt widely available to finance large leveraged buyouts. July and August saw a notable slowdown in issuance levels in the high yield and leveraged loan markets with only few issuers accessing the market. Uncertain market conditions led to a significant widening of yield spreads, which coupled with the typical summer slowdown led to many companies and investment banks to put their plans to issue debt on hold until the autumn. However, the expected rebound in the market after Labor Day

Labor Day

Labor Day is a United States federal holiday observed on the first Monday in September that celebrates the economic and social contributions of workers.-History:...

2007 did not materialize and the lack of market confidence prevented deals from pricing. By the end of September, the full extent of the credit situation became obvious as major lenders including Citigroup

Citigroup

Citigroup Inc. or Citi is an American multinational financial services corporation headquartered in Manhattan, New York City, New York, United States. Citigroup was formed from one of the world's largest mergers in history by combining the banking giant Citicorp and financial conglomerate...

and UBS AG

UBS AG

UBS AG is a Swiss global financial services company headquartered in Basel and Zürich, Switzerland, which provides investment banking, asset management, and wealth management services for private, corporate, and institutional clients worldwide, as well as retail clients in Switzerland...

announced major writedowns due to credit losses. The leveraged finance markets came to a near standstill. As 2007 ended and 2008 began, it was clear that lending standards had tightened and the era of "mega-buyouts" had come to an end. Nevertheless, private equity continues to be a large and active asset class and the private equity firms, with hundreds of billions of dollars of committed capital from investors are looking to deploy capital in new and different transactions.

Rationale

The purposes of debt financing for leveraged buyouts are twofold:- The use of debt increases (leverages) the financial return to the private equityPrivate equityPrivate equity, in finance, is an asset class consisting of equity securities in operating companies that are not publicly traded on a stock exchange....

sponsor. Under the Modigliani-Miller theoremModigliani-Miller theoremThe Modigliani–Miller theorem forms the basis for modern thinking on capital structure. The basic theorem states that, under a certain market price process , in the absence of taxes, bankruptcy costs, agency costs, and asymmetric information, and in an efficient market, the value of a firm is...

, the total return of an asset to its owners, all else being equal and within strict restrictive assumptions, is unaffected by the structure of its financing. As the debt in an LBO has a relatively fixed, albeit high, cost of capital, any returns in excess of this cost of capital flow through to the equity. - The tax shieldTax shieldA tax shield is the reduction in income taxes that results from taking an allowable deduction from taxable income. For example, because interest on debt is a tax-deductible expense, taking on debt creates a tax shield...

of the acquisition debt, according to the Modigliani-Miller theoremModigliani-Miller theoremThe Modigliani–Miller theorem forms the basis for modern thinking on capital structure. The basic theorem states that, under a certain market price process , in the absence of taxes, bankruptcy costs, agency costs, and asymmetric information, and in an efficient market, the value of a firm is...

with taxes, increases the value of the firm. This enables the private equity sponsor to pay a higher price than would otherwise be possible. Because income flowing through to equity is taxed, while interest payments to debt are not, the capitalized value of cash flowing to debt is greater than the same cash stream flowing to equity.

Germany

Germany

Germany , officially the Federal Republic of Germany , is a federal parliamentary republic in Europe. The country consists of 16 states while the capital and largest city is Berlin. Germany covers an area of 357,021 km2 and has a largely temperate seasonal climate...

currently introduces new tax laws, taxing parts of the cash flow before debt interest deduction. The motivation for the change is to discourage leveraged buyouts by reducing the tax shield effectiveness.

Historically, many LBOs in the 1980s and 1990s focused on reducing wasteful expenditures by corporate managers whose interests were not aligned with shareholders. After a major corporate restructuring, which may involve selling off portions of the company and severe staff reductions, the entity would likely be producing a higher income stream. Because this type of management arbitrage

Arbitrage

In economics and finance, arbitrage is the practice of taking advantage of a price difference between two or more markets: striking a combination of matching deals that capitalize upon the imbalance, the profit being the difference between the market prices...

and easy restructuring has largely been accomplished, LBOs today focus more on growth and complicated financial engineering to achieve their returns. Most leveraged buyout firms look to achieve an internal rate of return

Internal rate of return

The internal rate of return is a rate of return used in capital budgeting to measure and compare the profitability of investments. It is also called the discounted cash flow rate of return or the rate of return . In the context of savings and loans the IRR is also called the effective interest rate...

in excess of 20%.

Management buyouts

A special case of a leveraged acquisition is a management buyoutManagement buyout

A management buyout is a form of acquisition where a company's existing managers acquire a large part or all of the company.- Overview :Management buyouts are similar in all major legal aspects to any other acquisition of a company...

(MBO), which occurs when a company's managers buy or acquire a large part of the company. The goal of an MBO may be to strengthen the managers' interest in the success of the company. In most cases when the company is initially listed, the management will then make it private. MBOs have assumed an important role in corporate restructurings beside mergers and acquisitions

Mergers and acquisitions

Mergers and acquisitions refers to the aspect of corporate strategy, corporate finance and management dealing with the buying, selling, dividing and combining of different companies and similar entities that can help an enterprise grow rapidly in its sector or location of origin, or a new field or...

. Key considerations in an MBO are fairness to shareholders, price, the future business plan

Business plan

A business plan is a formal statement of a set of business goals, the reasons why they are believed attainable, and the plan for reaching those goals. It may also contain background information about the organization or team attempting to reach those goals....

, and legal and tax issues. One recent criticism of MBOs is that they create a conflict of interest—an incentive is created for managers to mismanage (or not manage as efficiently) a company, thereby depressing its stock price, and profiting handsomely by implementing effective management after the successful MBO, as Paul Newman's character attempted in the Coen brothers' film The Hudsucker Proxy

The Hudsucker Proxy

The Hudsucker Proxy is a 1994 screwball comedy film written, produced, and directed by Joel and Ethan Coen. Sam Raimi co-wrote the script and served as second unit director....

.

Of course, the incentive to artificially reduce share price extends beyond management buyouts.

It may be fairly easy for a top executive to reduce the price of his/her company's stock - due

to information asymmetry

Information asymmetry

In economics and contract theory, information asymmetry deals with the study of decisions in transactions where one party has more or better information than the other. This creates an imbalance of power in transactions which can sometimes cause the transactions to go awry, a kind of market failure...

. The executive can accelerate accounting of expected expenses, delay accounting of expected revenue, engage in off balance sheet transactions to make the company's profitability appear temporarily poorer, or simply promote and report severely conservative (e.g. pessimistic) estimates of future earnings. Such seemingly adverse earnings

news will be likely to (at least temporarily) reduce share price. (This is again due to information asymmetries since it is more common for top executives to do everything they can to window dress

their company's earnings forecasts).

A reduced share price makes a company an easier takeover

Takeover

In business, a takeover is the purchase of one company by another . In the UK, the term refers to the acquisition of a public company whose shares are listed on a stock exchange, in contrast to the acquisition of a private company.- Friendly takeovers :Before a bidder makes an offer for another...

target. When the company gets bought out (or taken private) - at a dramatically lower price - the takeover

Takeover

In business, a takeover is the purchase of one company by another . In the UK, the term refers to the acquisition of a public company whose shares are listed on a stock exchange, in contrast to the acquisition of a private company.- Friendly takeovers :Before a bidder makes an offer for another...

artist gains a windfall from the former top executive's actions to surreptitiously reduce share price. This can represent tens of billions of dollars (questionably) transferred from previous shareholders to the takeover artist. The former top executive is then rewarded with a golden parachute

Golden parachute

A golden parachute is an agreement between a company and an employee specifying that the employee will receive certain significant benefits if employment is terminated. Sometimes, certain conditions, typically a change in company ownership, must be met, but often the cause of termination is...

for presiding over the firesale that can sometimes be in the hundreds of millions of dollars for one or two years of work.

(This is nevertheless an excellent bargain for the takeover artist, who will tend to benefit from developing a reputation of being very generous to parting top executives).

Similar issues occur when a publicly held asset or non-profit organization undergoes privatization

Privatization

Privatization is the incidence or process of transferring ownership of a business, enterprise, agency or public service from the public sector to the private sector or to private non-profit organizations...

.

Top executives often reap tremendous monetary benefits when a government owned or non-profit entity

is sold to private hands. Just as in the example above, they can facilitate this process by making the

entity appear to be in financial crisis - this reduces the sale price (to the profit of the purchaser), and makes non-profits and governments more likely to sell. Ironically, it can also contribute to a public perception that private entities are more efficiently run reinforcing the political will to sell of public assets.

Again, due to asymmetric information, policy makers and the general public see a government owned firm

that was a financial 'disaster' - miraculously turned around by the private sector (and typically resold) within a few years.

Nevertheless, the incentive to artificially reduce the share price of a firm is higher

for management buyouts, than for other forms of takeovers or LBOs.

Failures

Some LBOs in the 1980s and 1990s resulted in corporate bankruptcyBankruptcy

Bankruptcy is a legal status of an insolvent person or an organisation, that is, one that cannot repay the debts owed to creditors. In most jurisdictions bankruptcy is imposed by a court order, often initiated by the debtor....

, such as Robert Campeau

Robert Campeau

Robert Campeau is a Canadian financier and real estate developer.-Early years:His formal education ended in grade eight, at the age of 14. He talked himself into jobs at Inco as a general labourer, carpenter and machinist. In 1949 he entered the residential end of the construction business...

's 1988 buyout of Federated Department Stores

Federated Department Stores

Macy's, Inc. is a department store holding company and owner of Macy's and Bloomingdale's department stores. Macy's Inc.'s stores specialize mostly in retail clothing, jewelery, watches, dinnerware, and furniture....

and the 1986 buyout of the Revco

Revco

Revco Discount Drug Stores , once based in Twinsburg, Ohio, was a major drug store chain operating through the Ohio Valley, the Mid-Atlantic states, and the Southeastern United States. The chain's stock was traded on the New York Stock Exchange under the ticker RXR...

drug stores. The failure of the Federated buyout was a result of excessive debt financing, comprising about 97% of the total consideration, which led to large interest payments that exceeded the company's operating cash flow. In response to the threat of LBOs, certain companies adopted a number of techniques, such as the poison pill

Poison pill

A shareholder rights plan, colloquially known as a "poison pill", or simply "the pill" is a type of defensive tactic used by a corporation's board of directors against a takeover...

, to protect them against hostile takeovers by effectively self-destructing the company if it were to be taken over.

The inability to repay debt in an LBO can be caused by initial overpricing of the target firm and/or its assets. Because LBO funds often attempt to increase the value of an acquired company by liquidating certain assets or selling underperforming business units

Strategic business unit

In essence, the SBU is a profit making area that focuses on a combination of product offer and market segment, requiring its own marketing plan, competitor analysis, and marketing campaign.A Strategic Business Unit emerges at the cross-over between:...

, the bought-out firm may face insolvency

Insolvency

Insolvency means the inability to pay one's debts as they fall due. Usually used to refer to a business, insolvency refers to the inability of a company to pay off its debts.Business insolvency is defined in two different ways:...

as depleted operating revenues become insufficient to repay the debt. Over-optimistic forecasts of the revenues of the target company may also lead to financial distress

Financial distress

Financial distress is a term in Corporate Finance used to indicate a condition when promises to creditors of a company are broken or honored with difficulty. Sometimes financial distress can lead to bankruptcy...

after acquisition. Some courts have found that LBO debt constitutes a fraudulent transfer

Fraudulent conveyance

A fraudulent conveyance, or fraudulent transfer, is a civil cause of action. It arises in debtor/creditor relations, particularly with reference to insolvent debtors. The cause of action is typically brought by creditors or by bankruptcy trustees...

under U.S. insolvency law if it is determined to be the cause of the acquired firm's failure.

However, the Bankruptcy Code

Bankruptcy Code

Bankruptcy Code may refer to:*Bankruptcy in Canada*Bankruptcy in the United States or Title 11 of the United States Code *Bankruptcy in China*Bankruptcy in the United Kingdom...

includes a so-called "safe harbor" provision, preventing bankruptcy trustees from recovering settlement payments to the bought-out shareholders. In 2009, the U.S. Court of Appeals for the Sixth Circuit held that such settlement payments could not be avoided, irrespective of whether they occurred in an LBO of a public or private company.

Secondary buyouts

A secondary buyout is a form of leveraged buyout where both the buyer and the seller are private equity firms or financial sponsorFinancial sponsor

A financial sponsor is a term commonly used to refer to private equity investment firms, particularly those private equity firms that engage in leveraged buyout or LBO transactions....

s (i.e. a leveraged buyout of a company that was acquired through a leveraged buyout). A secondary buyout will often provide a clean break for the selling private equity firms and its limited partner investors. Historically, however, secondary buyouts were perceived as distressed sales by both seller and buyer, were considered unattractive by limited partner investors and were largely avoided.

The increase in secondary buyout activity in 2000s was driven in large part by an increase in capital in the leveraged buyout space. Often, selling private equity firms will pursue a secondary buyout for a number of reasons:

- Sales to strategic buyers and IPOs may not be possible for niche or undersized businesses.

- Secondary buyouts may generate liquidity more quickly than other routes (i.e., IPOs).

- Some kinds of businesses—e.g., those with relatively slow growth but which generate high cash flows—may be most appealing to private equity firms than they are to public stock investors or other corporations.

Often, secondary buyouts have been successful if the investment has reached an age where it is necessary or desirable to sell rather than hold the investment further or where the investment had already generated significant value for the selling firm.

Secondary buyouts differ from secondaries

Private equity secondary market

In finance, the private equity secondary market refers to the buying and selling of pre-existing investor commitments to private equity and other alternative investment funds....

or secondary market purchases

Private equity secondary market

In finance, the private equity secondary market refers to the buying and selling of pre-existing investor commitments to private equity and other alternative investment funds....

which typically involve the acquisition of portfolios of private equity assets including limited partnership stakes and direct investments in corporate securities.

LBO Analysis

An LBO analysis is designed to estimate the current value of a company to a financial buyerFinancial sponsor

A financial sponsor is a term commonly used to refer to private equity investment firms, particularly those private equity firms that engage in leveraged buyout or LBO transactions....

, based on the company's forecasted financial performance. LBO analysis typically builds upon a medium-term forecast (typical investment horizon for financial sponsors is 3–7 years) to project future operating results.

The analysis works similarly, in many respects, to a discounted cash flow

Discounted cash flow

In finance, discounted cash flow analysis is a method of valuing a project, company, or asset using the concepts of the time value of money...

. The analysis will project the debt repaid by the company during the forecast period and make assumptions about the multiple of earnings at which the business will be sold after a period of time. By targeting returns consistent with historical targets for private equity firms, the LBO analysis will provide an estimate of what purchase price a buyer would be willing to pay to achieve those returns.

In Art

LBOs form the basis of several cultural works. In addition to the aforementioned Barbarians at the Gate: The Fall of RJR NabiscoBarbarians at the Gate: The Fall of RJR Nabisco